Discover everything you need to know about the UK tax year including key deadlines, compliance requirements, and essential filing obligations.

- In this article

- 2025/26 tax year for LTDs

- Corporation tax deadlines for LTD companies

- Companies House filing requirements for LTDs

- PAYE and Payroll Deadlines for LTDs

- VAT registration and filing obligations

- Salary and dividend planning for LTD directors

- How ANNA helps Limited Companies handle taxes with ease

Running a limited company in the UK involves juggling numerous deadlines, including Corporation Tax, PAYE, VAT, annual accounts, dividend planning, and other financial obligations. Falling behind on any one of these can lead to fines, stress, or worse: your company getting struck off the register.

This comprehensive guide walks you through everything you need to know for the 2025/26 tax year, tailored specifically for LTD directors.

2025/26 tax year for LTDs

The UK personal tax year runs from 6 April 2025 to 5 April 2026. Your LTD’s accounting year, however, is typically based on your incorporation date and financial year-end. This is known as your Accounting Reference Date (ARD).

- You can change your ARD, but you must inform Companies House.

- HMRC’s Corporation Tax deadlines follow your accounting period, which may not match the tax year.

💡 Tip: Consider aligning your accounting year with the tax year for simpler planning. This can make it easier to manage dividends, Self Assessment, and Corporation Tax.

To align your accounting year with the tax year:

- Log in to Companies House WebFiling.

- Navigate to your company profile and choose "Change accounting reference date".

- Select a new date that ends on 5 April, or close to it.

- Submit the change. You’ll receive confirmation when the update has been approved.

Important rules:

- You can shorten your accounting period as often as you like.

- You can extend it once every five years, unless granted special permission.

Why it helps: Aligning the ARD with the tax year streamlines reporting. It keeps salary, dividends, expenses, Corporation Tax, and Self Assessment all within one annual window, making record-keeping and year-end planning much easier.

Corporation tax deadlines for LTD companies

Corporation Tax is one of the most important responsibilities for a limited company. If you're a director, it’s essential to know exactly what to do and when to avoid penalties.

✅ Step 1: Register for Corporation Tax

📅 Deadline: Within 3 months of starting business activity (not necessarily incorporation).

📌 What counts as business activity?

- Selling your first product or service

- Advertising or marketing your business

- Employing staff

- Renting an office or workspace

💡 How to do it:

Companies are now automatically registered for Corporation Tax when they incorporate, so you no longer need to register separately. After incorporation, HMRC will send your Unique Taxpayer Reference (UTR) and information about your Corporation Tax responsibilities to your company’s registered address.

✅ Why it matters: You won't receive reminders or filing notifications from HMRC unless you're registered. You also risk late-filing penalties if you miss deadlines.

✅ Step 2: Pay Corporation Tax

📅 Deadline: 9 months and 1 day after your accounting period ends.

📌 Example:

- Accounting period ends on 31 December 2025

- Corporation Tax must be paid by 1 October 2026

💡 How to pay:

- Log into your HMRC business account

- Pay by bank transfer, Direct Debit, or card

- Keep a record of the payment date for your files

⚠️ Late payments incur interest and may impact future HMRC relationships.

📝 Tip: Set reminders at the 6-month and 8-month mark after your accounting year ends to give yourself time to prepare and budget.

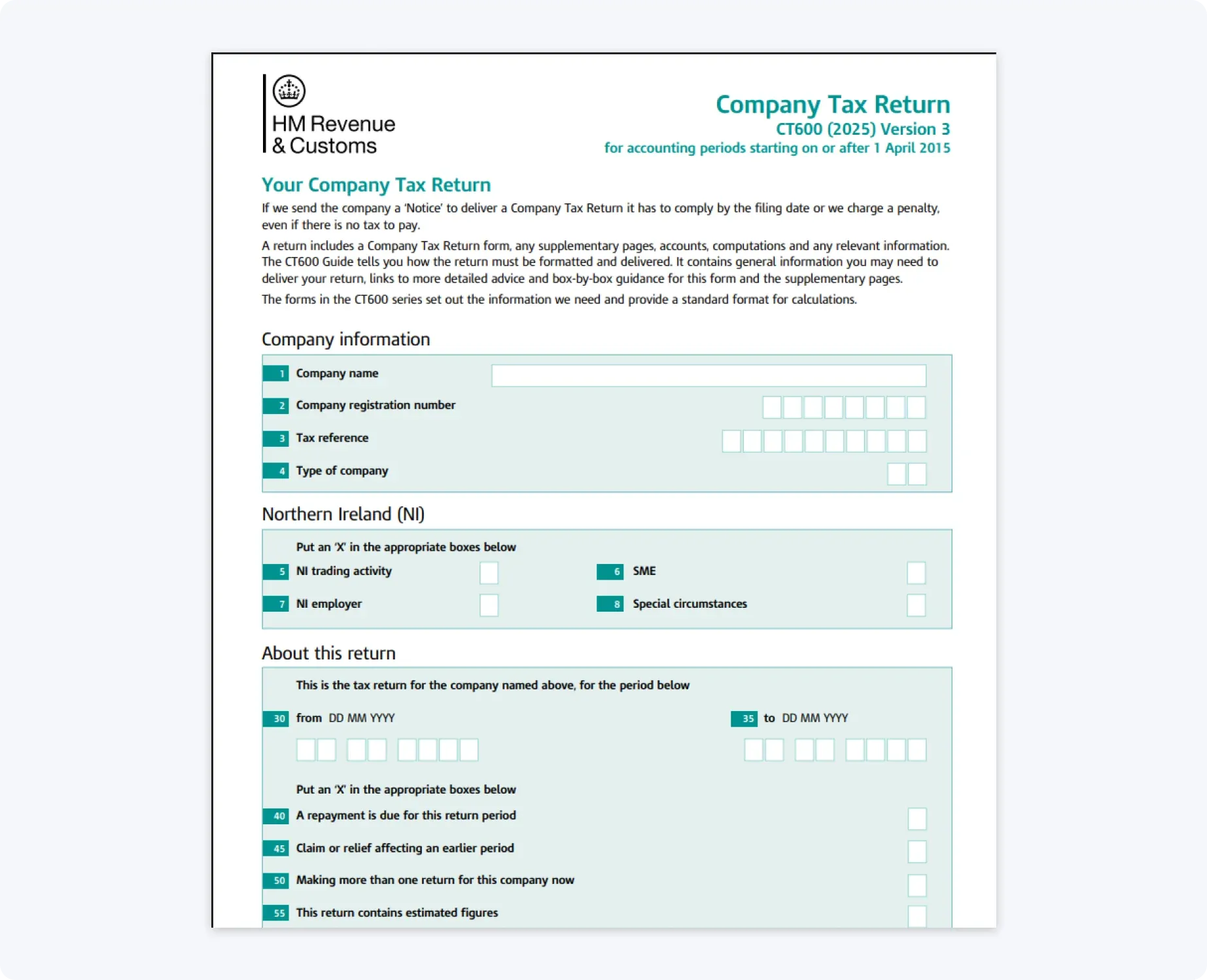

✅ Step 3: File Your Company Tax Return (CT600)

📅 Deadline: 12 months after the end of your accounting period.

📌 What you need to file:

- The CT600 form (main tax return)

- Full annual accounts (same as submitted to Companies House, plus notes)

- Detailed tax computations showing how your profit was calculated

💡 How to file:

- Use commercial accounting software or HMRC’s online service

- Most companies use an accountant, but you can do it yourself with the proper tools

⚠️ Don't confuse this with the payment deadline! Payment is due 9 months + 1 day after year-end; filing is due 12 months after year-end.

📉 Penalties for late filing:

- 1 day late: £100 fine

- 3 months: another £100

- 6 months: HMRC estimates your bill and adds 10%

- 12 months: an additional 10% of unpaid tax

✅ Tip: File as early as possible, especially if your profits are variable. You can amend a CT600 within 12 months if your situation changes.

Companies House filing requirements for LTDs

As a limited company, you’re legally required to submit specific information to Companies House every year. These filings are separate from your tax obligations with HMRC, but missing them can have serious consequences, including your company being struck off the register.

✅ Step 1: File Annual Accounts

📅 Deadline: Within 9 months of your accounting reference date (ARD).

📌 If it’s your first year in business: You get 21 months from incorporation to file your first accounts.

💡 What to include:

- Balance sheet

- Profit and loss statement

- Notes to the accounts

- Director’s report (for larger companies)

How to file:

- Submit online at Companies House WebFiling

✅ Tip: If your company qualifies as a micro-entity, you can file simpler accounts.

⚠️ Penalties for late filing:

If you miss the deadline two years in a row, the penalty doubles.

Even if your company is dormant or not trading, you still have to file accounts.

✅ Step 2: File the Confirmation Statement

📅 Deadline: Every year, within 14 days of the anniversary of your incorporation (or the last Confirmation Statement filed).

📌 What the statement confirms:

- Registered office address

- SIC code (business activity)

- Details of directors and secretary (if applicable)

- Shareholder information

- Persons with Significant Control (PSCs)

💡 How to file:

- Online via Companies House WebFiling

- It costs £13 to file online (£40 by post)

✅ Why it matters: The Confirmation Statement ensures Companies House has an up-to-date public record of your business. It doesn’t change your company details, but confirms they are accurate.

⚠️ Failure to file: Companies House can start proceedings to strike off your company. You may also face director disqualification.

📝 Tip: Keep track of changes throughout the year (like share transfers or new PSCs), so your confirmation statement is quick to update.

PAYE and Payroll Deadlines for LTDs

If your LTD company pays salaries, including to yourself as a director, you are required to operate PAYE (Pay As You Earn) and handle payroll reporting properly.

PAYE is the system HMRC uses to collect Income Tax and National Insurance from wages.

✅ Step 1: Register as an employer

📅 Deadline: You must register as an employer before your first payday.

📌 Who needs to register: Any LTD company that pays salaries, including sole-director companies paying a director’s wage.

💡 How to register:

- Visit www.gov.uk/register-employer

- Log in with your Government Gateway ID

- Complete the form with your company’s details

- HMRC will send you a PAYE reference and Accounts Office reference by post

✅ Why it matters: Registering ensures your company can legally run payroll and file real-time information (RTI) with HMRC. Without these references, you cannot meet your legal payroll obligations.

✅ Step 2: Run monthly Payroll and Submit RTI

📅 Deadline: Submit the FPS (Full Payment Submission) to HMRC on or before each payday.

📌 What you need to do each month:

- Use payroll software to calculate gross salary, Income Tax, employee and employer National Insurance

- Generate payslips for all employees and directors being paid

- Submit an FPS to HMRC using your payroll software

💡 Example: If your monthly payday is the 25th, then the FPS must be submitted by the 25th of each month.

✅ Recommended tools: Use HMRC-recognised payroll software like ANNA Payroll, Xero, QuickBooks, Sage, or FreeAgent to streamline the process.

⚠️ Penalties: HMRC imposes fines for late RTI filings. These start from £100 per month and can increase depending on the number of employees. Frequent delays or errors may trigger compliance reviews.

✅ Step 3: Pay PAYE and NIC to HMRC

📅 Deadline: You must pay PAYE and NIC by the 22nd of each month if paying electronically, or by the 19th if paying by post.

📌 What you must pay includes:

- Income Tax withheld from salaries

- Employee National Insurance contributions

- Employer National Insurance contributions

💡 How to pay:

- Log into your HMRC PAYE online account

- Make payment using bank transfer, Direct Debit, or the HMRC payment portal

- Always include your Accounts Office reference number when making payment

✅ Why it matters: Late payments automatically accrue interest. Persistent delays may affect your company’s tax compliance status with HMRC.

📝 Tip: Use your payroll software’s PAYE summary to double-check amounts due each month. Some directors choose to schedule a standing order around the 18th to avoid last-minute issues.

VAT registration and filing obligations

If your LTD company sells taxable goods or services, you may need to register for VAT. Even if your turnover is below the registration threshold, voluntary registration can still be advantageous, especially if your business regularly incurs VAT on purchases or deals with VAT-registered clients.

✅ Step 1: Check if you must register for VAT

📅 When to register: You must register for VAT if your VAT-taxable turnover exceeds £90,000 (2025/26 threshold) in any rolling 12-month period.

📌 What counts as taxable turnover:

- Income from the sale of goods or services subject to VAT

- Most consultancy, freelance, or professional services

- Online or physical product sales, even if only in the UK

💡 How to check your turnover:

- Use a spreadsheet or accounting software to monitor monthly turnover

- Add up sales from the past 12 months on a rolling basis (not calendar year)

- If you expect to exceed £90,000 in a single 30-day period, you must register immediately

✅ Voluntary VAT registration:

- You can register voluntarily below the threshold to reclaim VAT on expenses.

- This is useful for startups with significant setup costs or B2B businesses

✅ Step 2: Register for VAT

📅 Deadline: You must register within 30 days of exceeding the threshold or expecting to exceed it.

💡 How to register:

- Go to www.gov.uk/vat-registration

- Log in using your Government Gateway credentials

- Choose your VAT accounting scheme (Standard, Flat Rate, Cash Accounting, or Annual Accounting)

- Submit your business details and wait for your VAT number

Or, use ANNA to register for VAT, simple and stress-free with expert guidance, plus ongoing support for bookkeeping, automated VAT returns, and smart tax-saving features like Pots.

📌 What happens next:

- You’ll receive a VAT certificate with your registration date and VAT number

- You must update your invoices to include your VAT number

- You may need to backdate VAT charges to the date you became liable

✅ Why it matters: Delayed registration can result in backdated VAT liability that you’ll need to pay from your own funds if you didn’t charge customers VAT.

✅ Step 3: Submit VAT returns and make payments

📅 Deadline: Your VAT return is due one calendar month and 7 days after the end of each VAT quarter.

📌 Example:

- VAT quarter ends 30 June 2026

- VAT return and payment due by 7 August 2026

💡 How to file:

- Submit using Making Tax Digital (MTD)-compliant software (e.g., Xero, FreeAgent, QuickBooks)

- Keep digital records of all sales and expenses

- Ensure your return includes the correct VAT reclaimed and collected

✅ Recommended setup:

- Automate calculations using your software

- Set calendar alerts for each VAT quarter

- Check reconciliation monthly, so quarter-end isn’t rushed

⚠️ Late VAT penalties:

HMRC uses a points-based penalty system

- One late return = 1 penalty point

- Reaching 4 points results in an automatic £200 fine

- Late payments also incur interest

📝 Tip: Set up a dedicated VAT savings account and put aside around 20% of your VAT-able income. This helps ensure you have enough funds to pay your VAT bill when it's due.

ANNA has the Pots feature that automatically saves for your tax bill every time you get paid, so you don’t have to set any reminders.

Salary and dividend planning for LTD directors

One of the main advantages of running a limited company is the ability to pay yourself through a combination of salary and dividends. When structured correctly, this can reduce your overall tax liability while ensuring you're contributing to your National Insurance record and pension.

✅ Step 1: Decide on your director’s salary

📅 When to review: At the start of the tax year (April 2025) or when business circumstances change.

📌 Typical strategy for 2025/26: Many directors pay themselves a salary equal to the NIC Primary Threshold, which is £12,570 per year, or £1,047.50 per month.

💡 Why this amount works well:

- It keeps your salary within the tax-free Personal Allowance

- You don’t pay Income Tax, but still build qualifying years for your State Pension

- It reduces your Corporation Tax liability, as salary is a deductible business expense

✅ How to pay it:

- Run your salary through PAYE each month

- File your FPS (Full Payment Submission) via payroll software

- Make any necessary NIC or PAYE payments if you exceed thresholds

⚠️ Employer NIC liability kicks in above the Secondary Threshold (£9,100 for 2025/26). However, most LTDs qualify for the £5,000 Employment Allowance, unless the only employee is a director.

📝 Tip: If you're a sole director with no other employees, the Employment Allowance won’t apply. In that case, keep your salary below the NIC Secondary Threshold to avoid Employer NIC.

✅ Step 2: Pay yourself dividends

📅 When to issue dividends: Only from post-tax company profits, and only after preparing proper dividend paperwork.

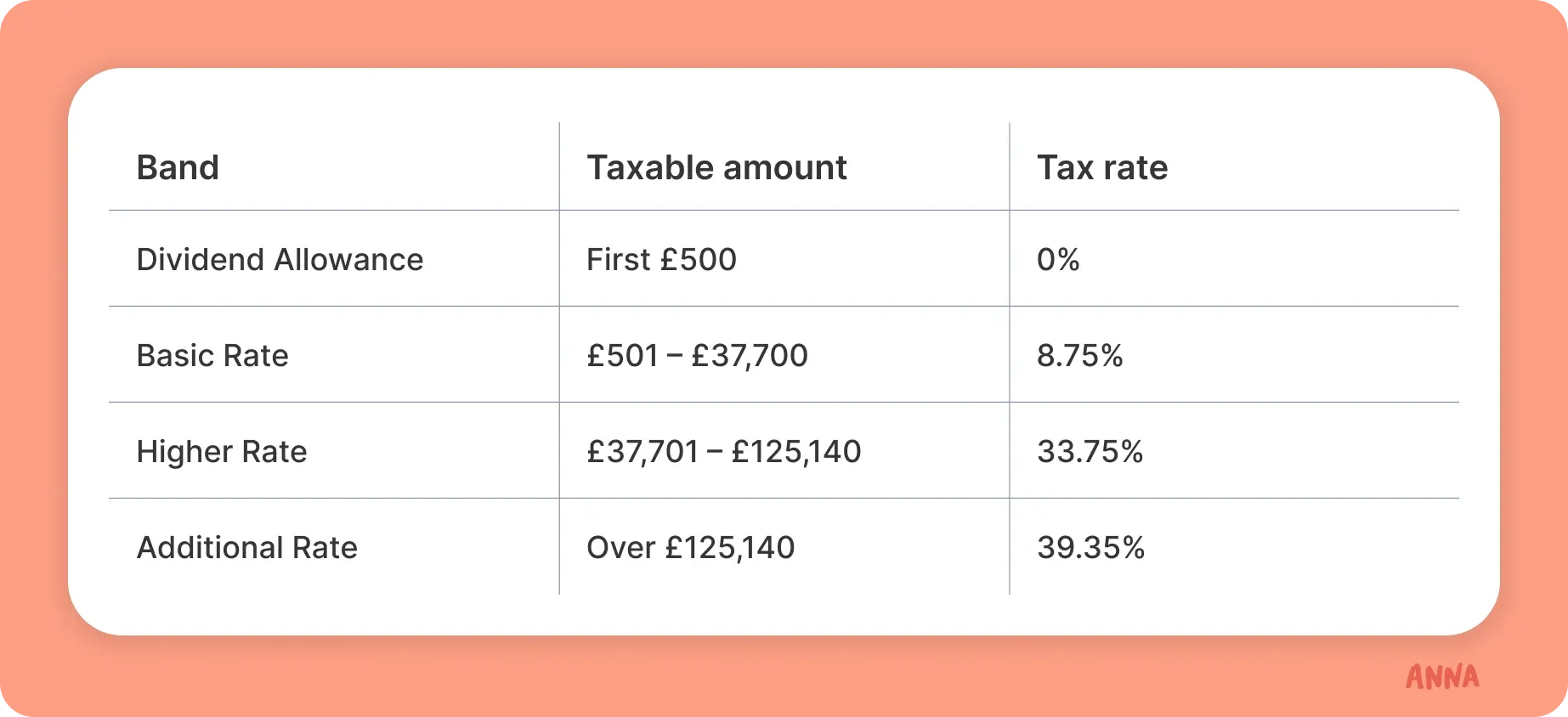

📌 Dividend tax rates for 2025/26:

💡 How to pay dividends:

- Ensure your company has retained profits (after Corporation Tax)

- Hold a board meeting (even if you're the only director)

- Prepare a dividend voucher showing: recipient, date, amount

- Record it in your accounting software

✅ Why dividends are tax-efficient:

- No National Insurance contributions apply

- You only pay dividend tax on amounts over the £500 allowance

- Paired with a low salary, it reduces total tax and NIC outgoings

⚠️ You can’t pay dividends if your company doesn’t have post-tax profits. Doing so could result in unlawful dividends and director loan issues.

📝 Tip: Many directors take a £12,570 salary plus around £37,700 in dividends to stay within the basic rate tax band. This keeps your marginal rate low while still drawing a healthy income.

✅ Step 3: File a Self Assessment tax return

📅 Deadline:

- Paper filing: 31 October 2026

- Online filing: 31 January 2027

📌 You must file if:

- You received dividends over £500

- Your total income exceeded the Personal Allowance

- You’re a director (unless you have no other untaxed income)

💡 What to include:

- Total salary paid via PAYE

- Total dividends received

- Any other personal income (e.g., rental income, interest)

✅ Why it matters: HMRC uses your return to calculate any dividend tax due. Failing to declare dividends correctly can result in penalties or backdated tax demands.

How ANNA helps Limited Companies handle taxes with ease

If you run a UK limited company, staying compliant with HMRC and Companies House is non-negotiable, but it doesn't have to be stressful. ANNA +Taxes and ANNA Payroll give LTDs a smarter way to manage taxes, payroll, and filings, all in one place.

Key Features for Limited Companies

1. All-in-one tax support ✔️ Register for VAT, PAYE, and Corporation Tax based on your LTD’s needs ✔️ Auto-calculate and file VAT Returns, PAYE, and Corporation Tax to HMRC ✔️ File Confirmation Statements (CS01) directly to Companies House 2. Smart expense tracking and tax-saving tools ✔️ Snap receipts and match them to transactions automatically ✔️ Expenses are auto-categorised to help you claim more and save more ✔️ Use Bookkeeping Score to stay on top of records and improve tax efficiency

3. Automated tax planning and reminders ✔️ Tax Pots put money aside automatically for VAT, PAYE, and Corporation Tax ✔️ Personalised tax calendar ensures you never miss a filing deadline ✔️ Get deadline alerts and keep records organised—all in your ANNA dashboard

4. Easy, HMRC-recognised payroll software ✔️ Run payroll for directors and up to 5 employees ✔️ Generate and store payslips, P45, and P60 automatically ✔️ Calculate and file NIC, pension contributions, and student loans seamlessly

5. Expert help at your fingertips ✔️ Ask Tax Terrapin, ANNA’s AI taxbot, any LTD-specific tax question ✔️ 24/7 expert support and links to official HMRC guidance ✔️ Fully HMRC- and Companies House-compliant tools 6. Professional invoicing and payments ✔️ Create branded invoices with payment links and QR codes ✔️ Accept card payments and manage transactions easily ..and so much more!

Pricing that grows with you

- ANNA +Taxes: £3/month for 3 months, then £24/month + VAT

- ANNA Payroll: £3/month for 3 months, then £20/month + VAT

- Add extra employees for just £5/month

With ANNA, your LTD can save time, reduce costs, and stay 100% compliant, all while running your business more efficiently.

From your first filing to ongoing payroll and tax management, ANNA gives you the tools and confidence to handle it all.

Read the latest updates

![9 Features to Look for When Choosing MTD Software [+Steps]](https://storage.googleapis.com/anna-website-cms-prod/small_cover_3000_32_ec1954cac9/small_cover_3000_32_ec1954cac9.webp)

![Making Tax Digital Costs: What Will MTD Cost You? [Breakdown]](https://storage.googleapis.com/anna-website-cms-prod/small_cover_3051_a896b063b0/small_cover_3051_a896b063b0.webp)

![Offshore Company Registration in the UK [2026 Guide]](https://storage.googleapis.com/anna-website-cms-prod/small_cover_3000_cdb14668f7/small_cover_3000_cdb14668f7.webp)

You may also like

![How to Apply for More Time to File Your Company Accounts [+Pro Tips]](https://storage.googleapis.com/anna-website-cms-prod/small_cover_3000_How_to_apply_for_more_time_to_file_your_company_accounts_4fbc560852/small_cover_3000_How_to_apply_for_more_time_to_file_your_company_accounts_4fbc560852.webp)

![How to register for Corporation Tax in UK? [Step-by-step Guide]](https://storage.googleapis.com/anna-website-cms-prod/22391eac_9a5e_41e3_8d5a_61ccf331d395_2023_04_18_Corporation_tax_and_LTD_a9e5d074fa/22391eac_9a5e_41e3_8d5a_61ccf331d395_2023_04_18_Corporation_tax_and_LTD_a9e5d074fa.avif)

Open a business account in minutes