Self Assessment Tax Return Deadlines & Processes [Explained]

Learn more about Self Assessment tax deadlines to stay compliant, avoid penalties, plan ahead with confidence, and make tax filing far less stressful.

In this article

If you’re self employed, a landlord, or earning income outside PAYE, there’s one date that is inevitable every year: your Self Assessment deadline.

Read on to learn more about Self Assessment tax return deadlines and avoid any issues with HM Revenue and Customs (HMRC).

Key points

- The UK tax year runs from 6th April to 5th April 📆

All income earned in this period, including self-employment, rental income, dividends, and capital gains, belongs to that tax year. - Registration and filing deadlines are crucial 🗂️

New Self Assessment filers must register by 5th October. Paper returns are due on 31st October, while online returns and payments are due on 31st January, with a 30th December option for PAYE collection. Missing these dates can result in penalties and interest. - Payments on account can surprise the unprepared 💷

If your tax bill exceeds £1,000, HMRC usually requires advance payments on account. The first is due on 31st January, and the second on 31st July. - Consistent record-keeping reduces stress 🧾

Keeping income, expenses, receipts, and invoices up to date prevents the chaos of January bookkeeping. Regular tracking gives you an accurate picture of your profits, identifies potential tax increases, and makes filing smoother. - Automating tax savings and filings makes life easier 💻

Using features like ANNA Money’s Money Pots to set aside tax and VAT funds ensures you never accidentally spend what you owe. ANNA also handles invoicing, bookkeeping, and filing Self Assessment, Corporation Tax, and VAT returns, making deadlines stress-free.

What is a tax year in the UK?

In the UK, the tax year doesn’t follow the calendar year. Instead, it runs from 6th April to 5th April the following year.

It feels a bit random, doesn’t it? Here’s a fun fact. The 6th April start date is actually a historical ‘leftover’ from calendar changes in the 1700s.

When Britain switched from the Julian to the Gregorian calendar in 1752, 11 days were effectively ‘lost.’

To keep tax revenues consistent, the tax year was shifted forward, and that’s why taxpayers still use 6th April today.

So, everything that you earn within that window belongs to that tax year. This includes self employed income, rental income, dividends, capital gains, and any other untaxed income.

If you’re self employed or earning untaxed income, the tax year determines:

- Which invoices belong in which return

- When you calculate your profit

- When the tax becomes due

- When payments on account are triggered

For example:

If you invoice a client on 4th April 2026, that income falls into the 2025/26 tax year. If you invoice on 7th April 2026, it goes into the 2026/27 tax year instead.

Just a few days can shift income into an entirely different return.

💡 Good to know:

You don’t file during the tax year – you file after it ends.

So, for the 2025/26 tax year (from April 2025 to April 2026), you earn money, and from April 2026 to January 2027, you report what you earned.

That gives you almost 10 months to file, but most people wait until January, which puts them on the clock and creates stress that could have been easily avoided.

4 key Self Assessment tax return deadlines

All of the dates below are set by HMRC and apply across the UK, each deadline serving a different purpose.

5th October: Registration deadline

This deadline only applies if you’re new to Self Assessment.

You need to register if you:

- Became self employed (sole traders)

- Became a partner in a partnership

- Started earning rental income

- Need to declare capital gains

- Began receiving significant untaxed income

If you’ve filed a Self Assessment before, you don’t need to register again.

Missing the registration deadline doesn’t automatically trigger a £100 fine, but it can cause problems later on:

- You may not receive your Unique Taxpayer Reference (UTR) in time

- You could struggle to file by 31st January

- Penalties may apply if late registration leads to late filing

31st October: Paper return deadline

If you’re still filing on paper, this is your deadline, and it’s three months before the online deadline.

Here are a few pointers:

- HMRC must receive your return by 31st October

- Posting it on the 31st isn’t enough

- Delays in the post won’t usually excuse a late filing

Paper returns are far less common now, but they’re still used in some situations, such as for complex returns or certain trusts.

However, filing online usually includes instant confirmation, automatic error checking, more time, and faster processing. Unless you have a specific reason for filing by mail, the online option is simpler and safer.

31st January: Online return and payment deadline

This is the big date because it’s both a filing deadline and a payment deadline.

By midnight on this date, you must:

- Submit your online Self Assessment return

- Pay any tax owed

- Make your first payment on account (if needed)

If you miss 31st January, you automatically get a £100 late filing penalty, interest begins on unpaid tax, and further penalties stack up over time.

January is extremely busy for accountants and HMRC systems, so waiting until the last week is risky.

💡 Quick tip:

You can file your return months in advance, from April onward, and still wait until 31st January to pay.

Filing early reduces stress, helps you budget, and prevents last-minute mistakes.

30th December: PAYE Tax code option deadline

If you owe less than £3,000 and want HMRC to collect it through your PAYE tax code instead of paying a lump sum, you must file your online return by 30th December.

This option spreads the tax you owe across the following tax year through slightly higher monthly PAYE deductions.

This is useful when:

- You’re employed and self employed

- You have a small side business

- You prefer not to pay everything in January

If you miss 30th December, you’ll need to pay the full amount by 31st January instead.

2 payment deadlines for the tax you owe

Besides filing deadlines, you should also keep payment deadlines in mind.

31st January: Balancing payment and first payment on account

On this date, you must pay:

- Your balancing payment: This is the tax you owe after subtracting any payments already made

- First payment on account: If your tax bill is over £1,000 and less than 80% of your tax is collected at source, HMRC usually requires advance payments toward the next tax year. This first payment on account is typically 50% of your previous year’s tax bill.

Because you need to pay a balancing payment and the first payment on account, January can feel like a financial shock if you’re unprepared.

31st July: Second payment on account

This date is when you usually pay the remaining 50% of the previous year’s tax bill.

For example, if you owe £4,000 for 2025/26, on 31st January 2027, you may need to pay a £4,000 balancing payment and a £2,000 first payment on account, totalling £6,000.

£2,000 would be due on 31st July 2027.

There’s no tax return due in July, just the payment, but many people tend to forget about this date because it arrives in the middle of the year.

💡 Quick tip:

If your income falls, you can apply to reduce your payments on account.

However, if you reduce them too much and underpay, HMRC may charge interest. So, reductions should be realistic and evidence-based.

3 practical tips to avoid missing Self Assessment tax return deadlines

Here are a few practical tips to help you stay comfortably ahead of every Self Assessment deadline:

1. Register early

If you’re newly self employed or earning untaxed income, registration is your first hurdle.

The deadline might be 5th October, but why wait until then?

When you register, HMRC needs to process your details, issue your UTR, and send activation codes for online filing. These things take time, especially during busy periods.

Instead, register as soon as you start trading. If you started freelancing in May, register in June.

2. Keep records throughout the year

January bookkeeping isn’t the wisest bookkeeping.

Trying to reconstruct 12 months of income and expenses from bank statements, invoices, and email searches is how mistakes happen.

You should make record-keeping small and consistent.

For example, once a month, reconcile income received, log business expenses, upload receipts, and update your mileage, if applicable.

Doing so also gives you a clearer picture of your profit, an early warning if your tax bill is growing, and better business decisions throughout the year.

Even though a basic spreadsheet is better than nothing, accounting software just makes it faster, easier, and error-free.

Did you know?

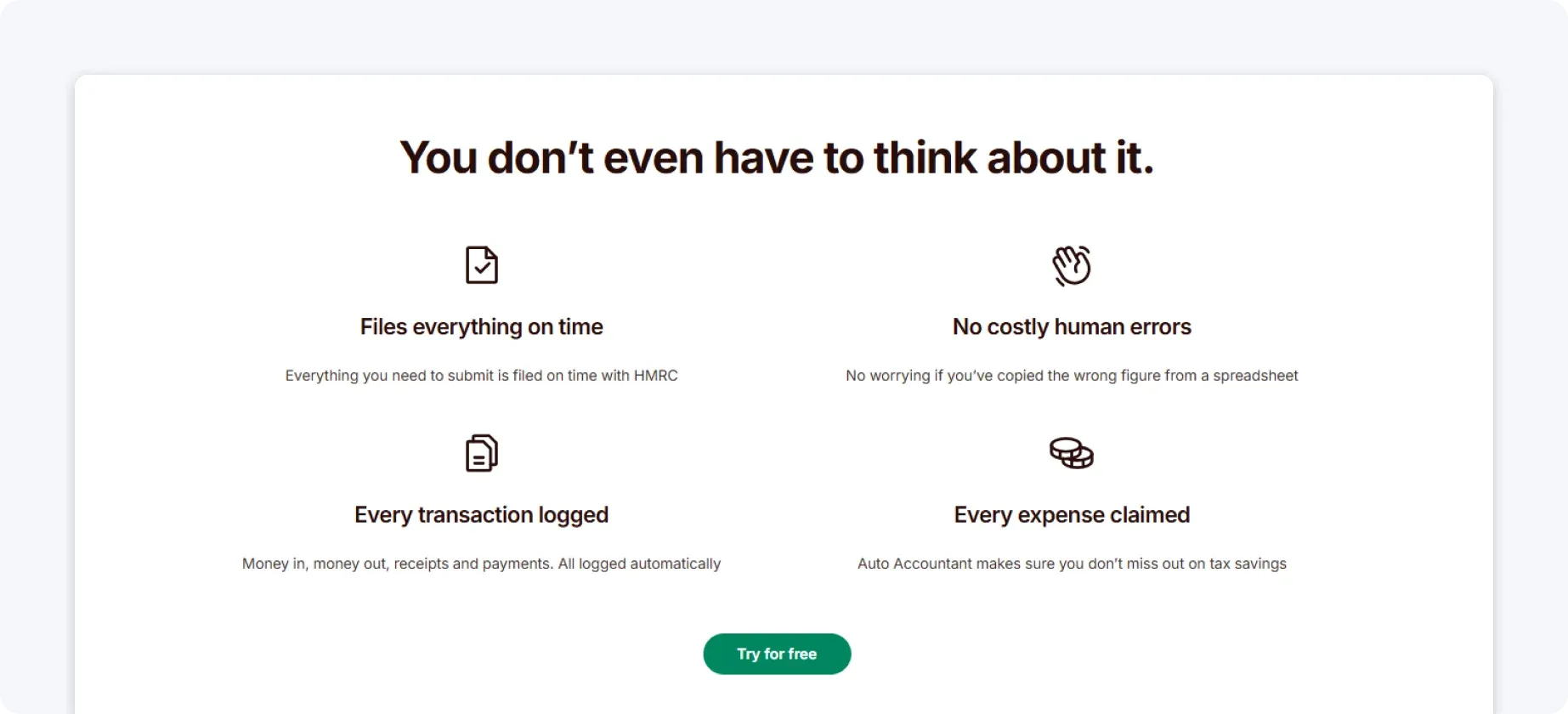

ANNA can help you with your tax return by keeping your books clean and tidy.

We safely store business documents, such as receipts, invoices, and tax reports, so your information is always at your fingertips.

Automatic invoice reconciliation means we can match your invoices with income payments and chase up anything that’s outstanding.

We’ll also sort out and categorise your business expenses so everything is in order, ready for your tax return.

3. Set aside tax monthly

The reason January feels painful usually isn’t the admin but the money.

When you’re self employed, no one deducts tax automatically. So it’s easy to treat all income as spendable.

Then January arrives, and suddenly you owe thousands. How can you avoid this inconvenient surprise?

Each time you’re paid, transfer a percentage into a separate savings account.

For example, you can set 20–30% for income tax, an additional amount if you are VAT registered, and an extra buffer for payments on account.

This way, when January comes, the money is already there.

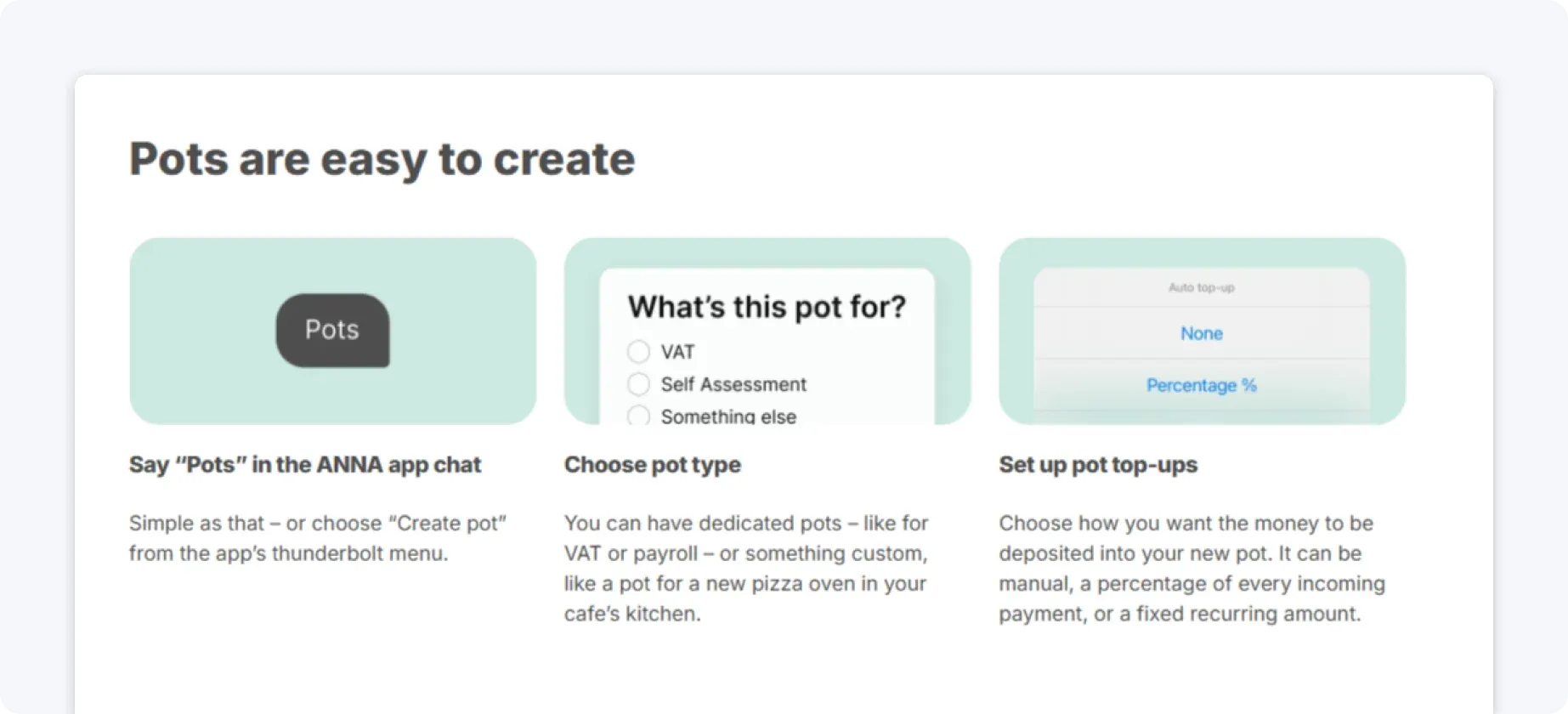

💡 Good to know:

Money Pots are a built-in feature of the ANNA business account that helps you organise your funds by setting money aside for specific purposes, such as tax bills, VAT, rent, bills, or savings goals, without needing separate accounts.

The money is part of your main account but is visually separated into labelled pots, so you always know what it’s reserved for.

You choose how money gets into a pot:

- Manual transfers

- A percentage of every incoming payment

- Fixed recurring amounts

You can also automate savings without thinking about the money.

When, for example, a tax bill is due, you can pay directly from the dedicated pot, so important payments don’t get mixed up with daily spending.

How to prepare for your Self Assessment tax return deadlines effortlessly with ANNA?

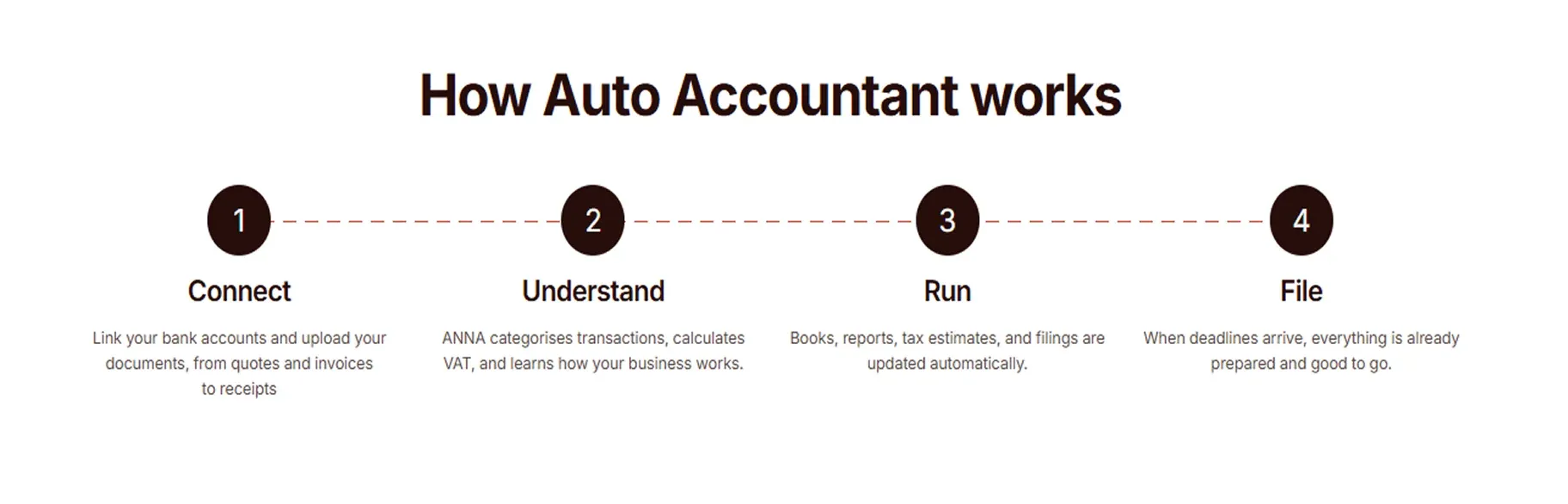

ANNA is an all-in-one business app that can register your business, send and chase invoices, handle your bookkeeping, and file your VAT, Corporation Tax, and MTD Self Assessment.

It’s built for business owners, not accountants, so there’s:

- No new software to learn: ANNA does everything for you

- No calculations or forms: Just answer a few simple questions

- No manual work: ANNA automatically collects data from your bank accounts, prepares your returns, and files them for you

Here’s what we do for you:

- Organise and maintain your finances 24/7: We keep documents safe and sorted, maintain accurate books, and provide up-to-date accounts at any time.

- Handle all major tax filings: We help you calculate tax efficiently and prepare and file Self Assessment, Corporation Tax, and VAT returns directly with HMRC.

- Manage payroll and PAYE: We take care of PAYE for your team and ensure compliance with HMRC requirements.

- Take care of company compliance: We deliver Year-End Financial Statements and submit Confirmation Statements to Companies House.

- Automate invoicing and tracking: We help you create invoices automatically and track them to help manage cash flow efficiently.

Ready to hand over your financial admin?

Try ANNA today to make your next Self Assessment deadline the easiest one yet.

FAQ:

1. Do I still need to file if I didn’t earn much or owe tax?

Even if you earned very little or don’t think you owe any tax, you still need to file a Self Assessment return if HMRC has told you to, or if your income meets the criteria.

You can check this with HMRC’s online tools (or software like ANNA) to eliminate guesswork and avoid missing a required return.

2. Do I need to file a tax return if I already pay tax through PAYE?

Sometimes, yes. Even if you’re employed and pay tax through PAYE, you may still need to file if you have additional income, such as freelance work, rental income, large dividends, or earnings over £100,000.

If you’re unsure, it’s best to check with HMRC rather than assume PAYE covers everything.

3. What if I can’t afford to pay my tax bill by 31st January?

If you can’t pay in full, don’t ignore it. HMRC offers a ‘Time to Pay’ arrangement, allowing you to spread the cost over monthly instalments.

Interest will still apply, but setting up a plan is far better than missing the deadline and facing escalating penalties.

4. What if I spot an error after filing?

If you spot an error after filing, you can amend your return within 12 months of the original deadline.

If you’ve overpaid tax, you can claim a refund online through your HMRC account. Make sure you keep all records and evidence for at least 5 years after the 31st January filing deadline in case HMRC asks for more details.

Read the latest updates

![How to Change Your Tax Code with HMRC in 2026 [Guide]](https://storage.googleapis.com/anna-website-cms-prod/small_cover_3079_44d1aec48c/small_cover_3079_44d1aec48c.webp)

![How to Avoid Paying Tax on Rental Income Legally? [Guide]](https://storage.googleapis.com/anna-website-cms-prod/small_cover_3000_91_8c2a5ee36e/small_cover_3000_91_8c2a5ee36e.webp)

You may also like

![How to Pay Corporation Tax to HMRC [Complete Guide]](https://storage.googleapis.com/anna-website-cms-prod/small_cover_3000_83_26707beab4/small_cover_3000_83_26707beab4.webp)

![What Is the BR Tax Code? [Full Meaning and Tax Impact]](https://storage.googleapis.com/anna-website-cms-prod/small_cover_3000_84_be2b800655/small_cover_3000_84_be2b800655.webp)

![Wrong Tax Code? How to Check and Fix It [Full Guide]](https://storage.googleapis.com/anna-website-cms-prod/small_cover_3000_89_8ed3de9f2b/small_cover_3000_89_8ed3de9f2b.webp)

![Tax on Savings: How Much Do You Pay? [Full 2026 Guide]](https://storage.googleapis.com/anna-website-cms-prod/small_cover_3000_81_647e3a3206/small_cover_3000_81_647e3a3206.webp)

Open a business account in minutes