Discover the advantages and disadvantages of a sole trader business including personal liability risks, taxes, and who this structure suits best.

- In this article

- What is a sole trader?

- Why do so many people in the UK choose sole trader status

- Advantages of being a sole trader in the UK

- Disadvantages of being a sole trader in the UK

- How personal liability works for sole traders

- Tax advantages and reliefs for sole traders

- Who becomes a sole trader in the UK?

- What influences job choice among sole traders?

- Do sole traders want to grow?

- Is it worth being a sole trader?

- How ANNA supports sole traders where it really counts

Becoming a sole trader is one of the most popular ways to run a business in the UK. With minimal paperwork, complete control, and simple tax requirements, it’s easy to see the appeal, especially if you’re striking out on your own for the first time.

But is it the right fit for everyone?

This guide explores all aspects of being a sole trader, including the advantages, disadvantages, risks to your personal assets, how taxes work, and the types of people who tend to thrive in this business model.

What is a sole trader?

In legal terms, a sole trader is an individual who owns and operates their business entirely on their own. There’s no distinction between the person and the business in the eyes of the law.

You’re responsible for everything: from sales and customer service to taxes and debts.

You don’t need to register with Companies House. All that’s required is registering with HMRC as self-employed, usually through the Self Assessment system. This simplicity is one of the main reasons people choose this route.

🔎 Read more about how to register as a sole trader in the UK in our blog!

Why do so many people in the UK choose sole trader status

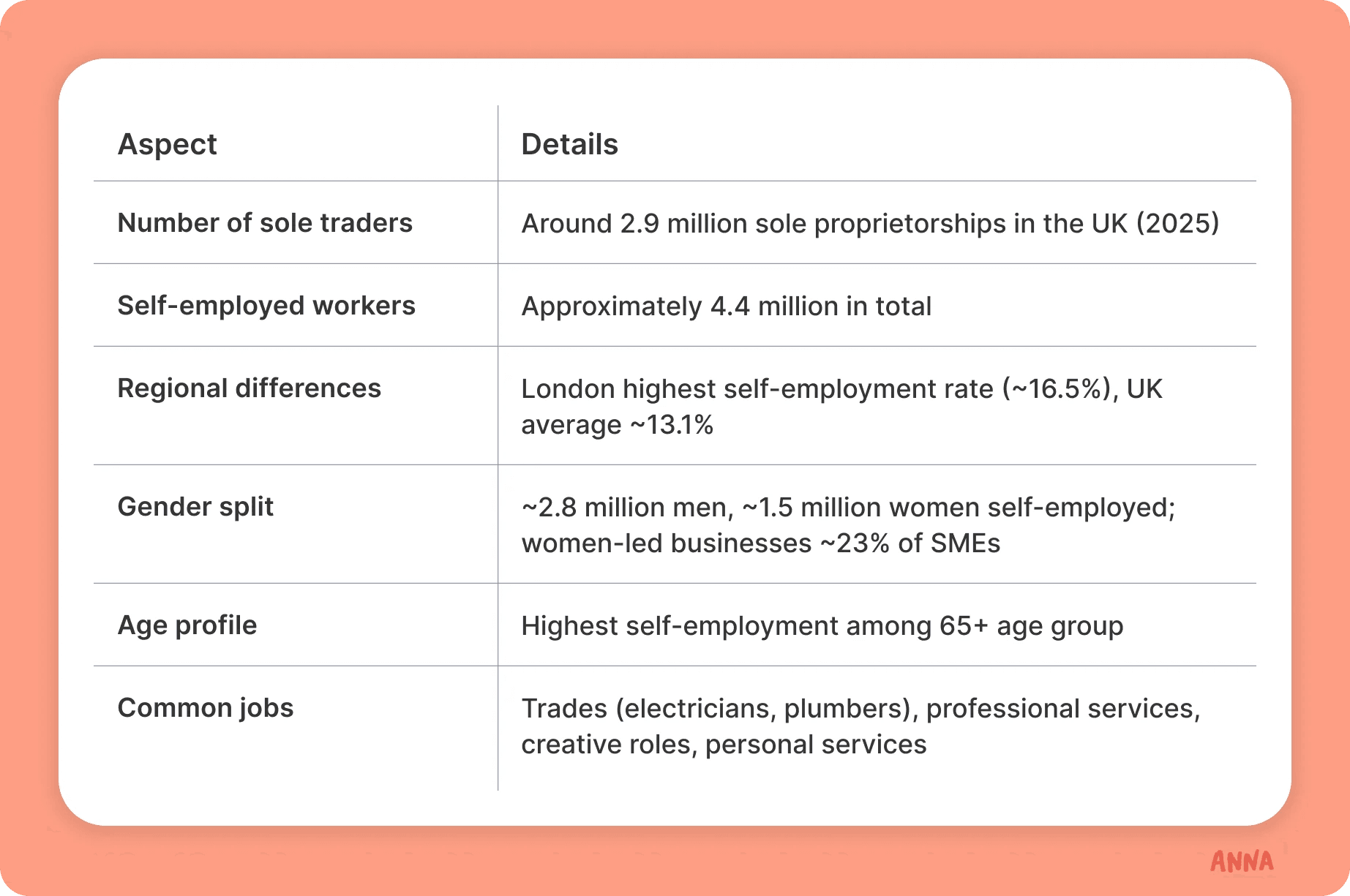

As of 2025, there are nearly 2.9 million sole proprietorships across the UK, making them the most common business structure in the country. The appeal is especially strong for freelancers, tradespeople, delivery drivers, and creatives, but you’ll also find consultants, small retailers, and fitness professionals among their ranks.

For many, it’s about lifestyle. Sole traders value independence. There’s no boss, no board, and no bureaucracy.

But what works well in one phase of your career may not suit you forever. That’s why understanding the full picture – advantages and disadvantages – is essential.

Advantages of being a sole trader in the UK

✅ Starting a business is fast and straightforward

When you decide to go it alone, you can get up and running in a matter of hours. There’s no need to file incorporation documents or appoint directors. A quick registration with HMRC and you’re officially self-employed.

That ease is ideal for anyone who wants to test a business idea without spending weeks on setup.

Example: If you’re a graphic designer, you could start freelancing with just a laptop and a few online platforms, without needing to register a company or pay incorporation fees.

✅ You control every business decision

As a sole trader, you have direct control over your business operations and can make decisions quickly without needing formal approval from others. This autonomy allows for flexibility to adapt your business as needed.

While limited companies also offer significant control, especially for owner-managed businesses, sole traders benefit from a simpler decision-making process with fewer formalities.

If you want to raise prices, change suppliers, switch services, or even close down entirely, you can do so without the need for board meetings or shareholder resolutions. This streamlined approach is a major reason many sole traders report high job satisfaction.

✅ You keep all the profits

As a sole trader, all profits your business makes (after tax) go directly to you – there’s no need to share income with other business owners or shareholders. This straightforward approach means your personal effort is closely tied to your financial reward.

In contrast, if you are the sole director and shareholder of a limited company, the profits belong to the company as a separate legal entity. You then extract these profits primarily through a combination of salary and dividends.

While you are entitled to 100% of the available profits as dividends if you are the only shareholder, this process involves specific administrative steps, such as holding directors' meetings (even if you are the only one) to declare dividends and preparing dividend vouchers. Dividends can only be paid from available profits after Corporation Tax and other liabilities have been paid, and while the company doesn't pay tax on dividend payments, shareholders may pay Income Tax on them above a certain threshold.

Many limited company directors opt for this method as it can be more tax-efficient than taking a large salary. The key distinction is the formal process of profit distribution and the separate tax implications for the company and the individual, unlike the direct retention of profits by a sole trader.

✅ You face lower ongoing costs

Sole traders aren’t required to file annual accounts to Companies House or maintain complex corporate records. Accounting and admin are simpler and cheaper.

While you’ll still need to track income and expenses accurately, the burden is lighter than what limited companies face.

✅ Tax is simpler (at least initially)

As a sole trader, you submit a Self-Assessment tax return annually and pay tax on your profits as personal income. There’s no corporation tax or dividend tax. You can also deduct business expenses from your income to reduce your tax bill.

You only need to register for VAT if your turnover exceeds the threshold (currently £90,000), which means many small businesses can avoid the extra paperwork entirely.

✅ Easier to build client relationships

Because you are the business, customers deal with you directly. That creates a personal connection, often leading to better customer loyalty and trust.

In sectors like trades or personal services, this personal touch can be a real competitive advantage.

Disadvantages of being a sole trader in the UK

❌ Your personal assets are at risk

This is perhaps the single biggest drawback: there is no legal boundary between your business and your personal finances. If you’re sued or go into debt, your house, car, and savings could be seized to repay creditors.

Example: If a client sues you for breach of contract and wins, and your business can’t cover the damages, your personal property could be at stake.

This liability also applies to unpaid tax. HMRC has broad powers to collect debt, including using enforcement officers to seize assets.

❗Mitigation options: Many sole traders take out public liability or professional indemnity insurance. Others switch to a limited company structure once the business grows.

❌ Building trust with suppliers or clients can be harder

Some businesses are hesitant to work with sole traders, especially on large contracts. They may assume your business is less stable or harder to scale. That can make it difficult to establish trade credit accounts, secure financing, or win bids.

The perception of professionalism, fair or not, can be lower than with limited companies.

❌ You may struggle to raise finance

Without shareholders, equity, or audited accounts, it’s tougher to attract investment. Banks are often wary of lending to sole traders because they see more risk and less transparency.

You can’t issue shares or offer equity in your business, which limits your options for raising capital.

Sole traders often have to rely on personal savings, credit cards, or loans based on personal income rather than business performance.

❌ Fewer tax planning tools

While tax is simpler, you don’t have access to some of the strategies available to company directors, like paying yourself through a combination of salary and dividends.

As a sole trader, you’re taxed on all profits at income tax rates. There’s no way to shelter income through dividend taxation or retain profits in the business for future use.

You can still reduce your bill through business expenses, capital allowances, and pension contributions, but advanced planning options are limited.

❌ You do everything yourself

Even if you outsource tasks like bookkeeping or design, the responsibility ultimately falls on your shoulders. You’re the manager, marketer, customer service rep, and finance director – all at once.

There’s no paid sick leave, no paid holidays, and no team to delegate to unless you hire contractors.

This workload can quickly lead to burnout, especially in seasonal or high-demand industries.

❌ Business ends with you

If you want to sell the business, retire, or pass it on, doing so can be complicated. Unlike a limited company, there’s no separate legal entity to sell or transfer.

If you stop working, the business usually stops too.

How personal liability works for sole traders

Let’s get specific. If your business owes money or loses a lawsuit, creditors can:

- Seize your personal bank accounts

- Force the sale of your home or car

- Initiate bankruptcy proceedings

- Bypass court processes (if HMRC is involved) and use bailiffs

This lack of legal separation is a serious financial risk. It’s why some sole traders convert to limited companies once turnover increases or they begin working with higher-risk clients.

However, you can reduce risk through:

- Insurance (e.g., public liability or indemnity)

- Setting up a limited company for protection

- Formal arrangements like Individual Voluntary Arrangements (IVAs)

Tax advantages and reliefs for sole traders

Sole traders pay tax through the Self Assessment system. Here’s what that means:

🔸 Income Tax instead of Corporation Tax: You only pay tax on your profits as personal income. There’s no separate tax on the business entity, which keeps reporting requirements simpler.

🔸 No double taxation: You don’t pay dividend tax on money you take out of the business because it’s already taxed as personal income.

🔸 Claim business expenses:

You can deduct costs such as:

- Travel (including mileage allowances)

- Equipment and supplies

- Utilities and home office expenses

- Phone and internet bills

- Marketing, insurance, bank charges (and this directly reduces your taxable profit.)

🔸 Loss relief: If your business makes a loss, you can offset it against other personal income, like employment or rental income, potentially reducing your tax bill in that year.

🔸Capital allowances: For larger purchases (e.g., vehicles, machinery), you can claim deductions over time to spread the cost.

Who becomes a sole trader in the UK?

The sole trader community is more diverse than you might think.

🔸 Age

Self-employment is highest among workers aged 65 and over. Many use it as a flexible transition into retirement.

🔸 Gender

Around 2.8 million men and 1.5 million women are self-employed. Women-led businesses account for 23% of all SMEs and are growing steadily, especially in personal services, design, wellness, and care sectors.

🔸 Regional trends

London has the highest rate of self-employment at 16.5%, well above the UK average of 13.1%. Urban centers tend to attract more freelancers and contractors, while rural areas often see more agricultural sole traders.

What influences job choice among sole traders?

Several factors affect the popularity of certain jobs among sole traders:

- Industry accessibility: Some sectors are easier to enter due to low capital requirements or minimal licensing (e.g., design, delivery).

- Stable demand: Health, property, and personal care roles tend to have consistent customer needs.

- Demographics: Older men often dominate trades, while women lead in wellness, education, and design.

- Economic trends: The rise in eCommerce and gig work has increased demand in logistics, delivery, and remote services.

- Income stability: Sectors with better five-year survival rates (health, finance) are more attractive long-term.

🔎 Thinking about starting a care agency? Don’t miss out on our blog!

Do sole traders want to grow?

Surprisingly, most don’t. Approximately 70% of sole traders report a preference for remaining small.

Why?

- They value independence more than income growth.

- Managing employees or scaling up can be stressful.

- Many prefer lifestyle businesses that fit their personal schedule and goals.

- Instead of growing in size, many adapt by using digital tools, diversifying their services, or outsourcing work to freelancers.

Is it worth being a sole trader?

There’s no one-size-fits-all answer. Being a sole trader offers freedom, simplicity, and full control, but it demands personal resilience, financial caution, and long-term planning.

Ideal for you if:

- You’re testing a business idea or freelancing

- You prefer to stay lean and nimble

- You don’t need outside investment (yet)

But reconsider if:

- You want to scale or take on staff

- You’re in a high-risk or high-debt industry

- Protecting personal assets is a priority

Many business owners start as sole traders and switch to a limited company later as their goals evolve.

So, is it worth it? Absolutely, for the right kind of person, at the right stage in their journey.

How ANNA supports sole traders where it really counts

Running your business solo doesn’t mean doing everything alone. ANNA gives sole traders practical tools that actually reduce the stress of managing money, without drowning you in jargon or admin.

- Open a business account in minutes – No branch visits, no paperwork pileups. Just your ID and a few taps.

- Sort expenses with your camera – Snap receipts and ANNA automatically reads and categorises them. No shoebox, no spreadsheets.

- Keep tax money where it belongs – Smart pots set aside funds for tax bills, so you’re not scrambling at the end of the year.

- Send invoices instantly (and chase late ones) – Create clean, professional invoices from your phone and let ANNA nudge the clients who haven’t paid.

- Get real-time estimates of what you owe HMRC – From VAT to corporation tax (if you go limited), ANNA keeps you ahead of deadlines.

- Give your accountant live access – Or connect to Xero and QuickBooks in seconds.

Alternatively, if you wish to take the next step and register as a limited company, ANNA can assist you for free.

Choose from flexible pricing plans tailored to your needs:

- Basic – Just £19 + VAT, includes your Companies House fee and quick company formation.

- Essential – Best for most businesses, now only £119/year + VAT (was £310), covering your company’s filings, tax submissions, and a business account with debit card.

- Privacy – £180/year + VAT, perfect for keeping your home address private with a professional London office address.

- Total Support – Great value at £395/year + VAT (worth £750), includes tax support, filings, prime address, business banking, and more.

Want to go further? Add services like VAT registration, PAYE setup, confirmation statement filing, and more – all available during signup.

Most business apps make life more complicated. ANNA does the opposite, especially for sole traders who just want to get paid, stay compliant, and keep things moving.

➡️ Open an ANNA account now – and let the app handle the boring bits while you run your business your way.

Read the latest updates

![What Is the Threshold for Making Tax Digital? [Guide]](https://storage.googleapis.com/anna-website-cms-prod/small_cover_3057_f0f2ffd268/small_cover_3057_f0f2ffd268.webp)

![Making Tax Digital for Freelancers [Complete 2026 Guide]](https://storage.googleapis.com/anna-website-cms-prod/small_cover_3000_25_15d6713572/small_cover_3000_25_15d6713572.webp)

![How to Sign Up for Making Tax Digital [A Detailed Guide]](https://storage.googleapis.com/anna-website-cms-prod/small_cover_3031_86f7f6f18a/small_cover_3031_86f7f6f18a.webp)

![MTD ITSA for Landlords [+6 Software Options Compared]](https://storage.googleapis.com/anna-website-cms-prod/small_cover_3025_77131ed4c8/small_cover_3025_77131ed4c8.webp)

![How to Choose the Best MTD Bridging Software [+Comparison]](https://storage.googleapis.com/anna-website-cms-prod/small_cover_3000_22_ba8f9dee9d/small_cover_3000_22_ba8f9dee9d.webp)

![How to Change from Sole Trader to Limited Company [10 Steps]](https://storage.googleapis.com/anna-website-cms-prod/small_Cover3000_Howto_Changefrom_Sole_Traderto_Limited_Company_2ad167a58b/small_Cover3000_Howto_Changefrom_Sole_Traderto_Limited_Company_2ad167a58b.png)

![Can Sole Traders Have Employees? [Rules Explained]](https://storage.googleapis.com/anna-website-cms-prod/small_cover_3000_Can_Sole_Traders_Have_Employees_Rules_Explained_0a5a2f5654/small_cover_3000_Can_Sole_Traders_Have_Employees_Rules_Explained_0a5a2f5654.webp)

Open a business account in minutes