Explore the disadvantages of partnership in the UK and understand key risks like liability, conflicts, and challenges before starting your business.

On paper, a partnership sounds perfect: shared workload, pooled resources, and someone to bounce ideas off.

However, despite its benefits, a partnership can also bring disadvantages. These include unlimited liability that puts your personal assets at risk, as well as conflicts over decision-making and profit-sharing.

That’s why you should understand the key disadvantages of partnership in the UK before entering this type of business arrangement.

What is a partnership in the UK context?

In the UK, a business partnership is basically when two or more people, or even companies, join forces to run a business and make a profit.

Legally, it’s defined under the Partnership Act 1890 as a relationship between people who are working together in a business with the goal of earning money.

Key characteristics of a UK partnership

- Number of partners: There must be at least two partners, which can be individuals or legal entities such as companies.

- Profit and loss sharing: Partners share the profits and losses of the business according to the terms of the partnership agreement, or equally if no agreement is made.

- Joint and several liability: Except in limited liability partnerships (LLPs), partners have unlimited personal liability for debts and obligations of the business. This means their personal assets can be used to pay business debts.

- Legal status: A partnership isn’t a separate legal entity from its partners, except LLPs. The partners are the business legally and are responsible for its actions and liabilities.

- Management and decision-making: Partners typically participate in managing the business and making decisions collectively.

- Partnership agreement: While not always legally mandatory, most partnerships operate under a formal partnership agreement that outlines roles, profit-sharing, dispute resolution, and procedures for adding or removing partners.

- Taxation: Partnerships don’t pay corporation tax. Instead, profits are passed through to partners and taxed as personal income.

- Business continuity: If one partner decides to leave, or sadly passes away, the partnership could come to an end, unless you’ve planned and put something in place to keep the business running.

This structure has a relatively simple and flexible formation and operation, making it popular for small to medium-sized businesses and professional firms in the UK.

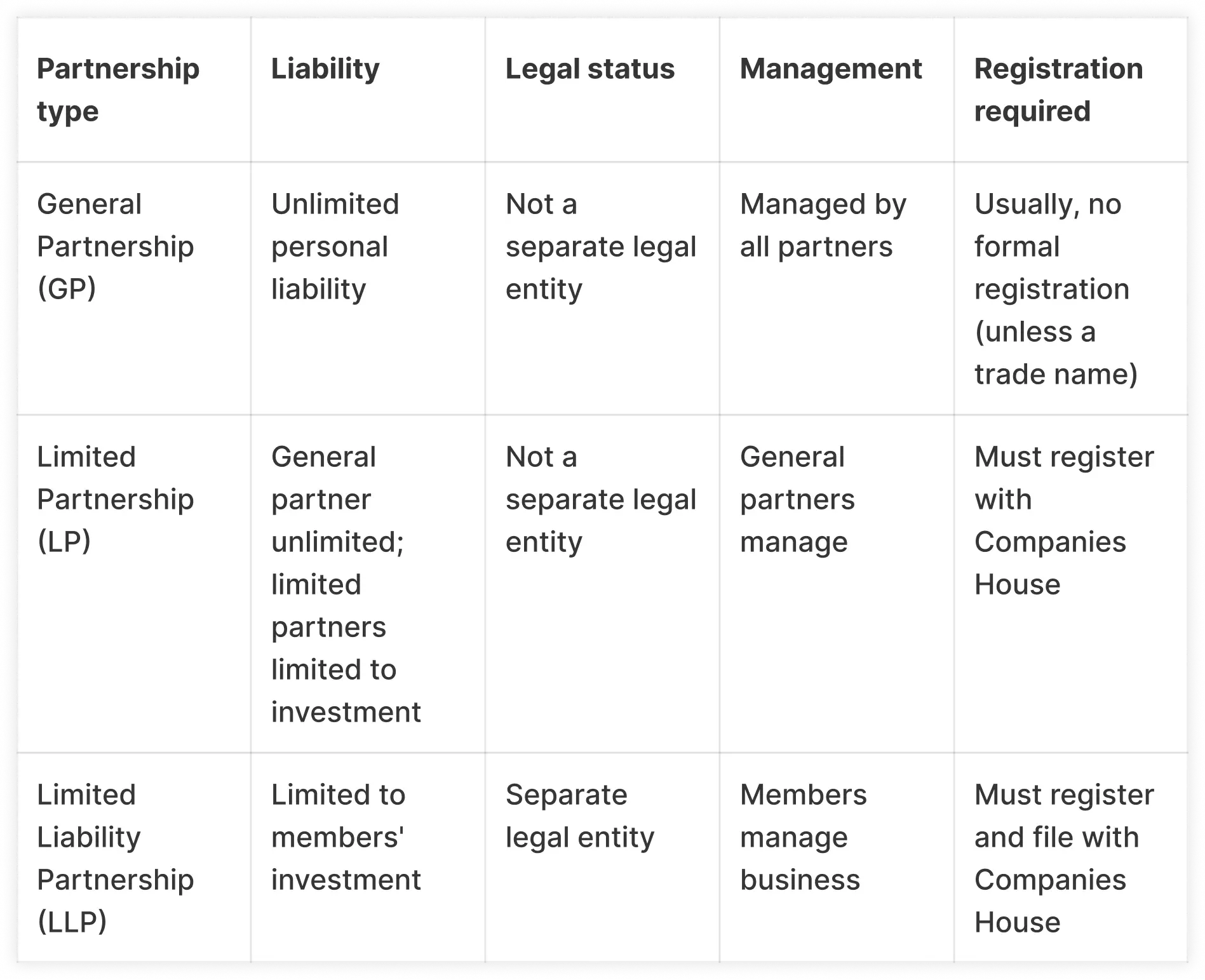

What are the main types of partnerships in the UK?

In the UK, partnerships come in a few different forms, each with its own rules, responsibilities, and level of liability.

Let’s look at the 3 main types you need to know about.

1. General Partnership (GP)

This is the most straightforward type of partnership. Everyone shares the responsibility for running the business, and that includes the risks.

Each partner has unlimited personal liability, which means if the business gets into debt, your personal assets could be on the line.

A GP isn’t a separate legal entity, so partners are jointly and severally liable for everything.

Usually, it’s set up by agreement and doesn’t require formal registration unless you’re trading under a specific business name.

Profits and losses are split based on your partnership agreement, or equally if you don’t have one.

2. Limited Partnership (LP)

An LP has at least one general partner who runs the business and carries unlimited liability, and one or more limited partners who invest money but have liability only up to the amount they put in.

Limited partners are usually silent investors, and they don’t get involved in day-to-day decisions.

Unlike a GP, an LP must be registered with Companies House. It’s not as popular these days, especially since LLPs came along.

3. Limited Liability Partnership (LLP)

An LLP is like a mix between a partnership and a company.

It’s a separate legal entity, which means the business is legally distinct from its members.

The biggest advantage is that members have limited liability, so their personal assets are protected if the business runs into trouble.

Members can manage the business without being personally liable beyond what they’ve invested.

LLPs have to register with Companies House and follow company filing rules.

For tax purposes, they’re treated as transparent entities, which means that profits pass through to the members, who then pay income tax personally.

Disadvantages of partnership in business in the UK: What you need to know

Before you shake hands on a business partnership, you may want to consider potential downsides.

1. Unlimited liability: Your personal assets are at risk

In a typical business partnership, each partner is personally responsible for the company’s debts and losses.

That means if the business runs into trouble or owes money, it’s not just the business at risk. Your personal savings, property, and other assets could be on the line.

What’s more, it’s not just your own decisions you need to worry about. If a partner makes a risky move, takes on debt, or signs a contract you weren’t aware of, you can still be held liable.

Unlimited liability is a big difference from limited companies, where the owners’ financial responsibility usually stops at the amount they’ve invested.

In a partnership, there’s no safety net. Your personal finances are tied directly to the business, for better or worse.

2. Lack of separate legal identity

One thing that may surprise a lot of new business owners is that a partnership isn’t legally separate from the people running it.

In plain English, that means the business and its partners are treated as the same entity under the law.

What does that actually mean for you?

Well, if a partner decides to quit, gets seriously ill, or, even worse, passes away, the partnership could automatically end unless you’ve already set up agreements to keep things running.

In other words, a thriving business can suddenly be derailed by changes in the partners.

This lack of continuity makes long-term planning somewhat challenging.

Unlike a limited company, which keeps going no matter who’s in charge, a partnership’s future can feel a little shaky if the right protections aren’t in place from day one.

It’s one of those hidden pitfalls that’s easy to ignore until it hits.

3. Profits are shared even if the effort isn’t equal

When you run a partnership, you don’t get to keep all the profits for yourself like a sole trader would. Instead, the earnings are shared among the partners.

That might sound fair on paper, but it can lead to tension, especially if one partner is putting in long hours while another contributes less, or if some invested more money than others.

The best way to avoid arguments is to have a clear partnership agreement that spells out exactly how profits and losses will be shared.

Getting this sorted from the start can save a lot of frustration and keep the business running smoothly.

4. Shared responsibility can lead to conflicts

At first, sharing the workload sounds great. But what happens when you disagree on big decisions?

In a partnership, you’re not the only one calling the shots. Every major decision has to be made together.

Maybe you want to reinvest profits, while your partner wants to take a bigger salary. Disagreements like these can strain the relationship and slow things down, and in some cases, break the business.

Reaching an agreement often means a lot of negotiation and compromise, which can be frustrating and time-consuming.

And sometimes, that delay can even cause you to miss out on opportunities that move quickly.

5. Limited growth options

Partnerships can be great for starting a business with someone you trust, but when it comes to growing the business, things can get tricky.

Unlike limited companies, partnerships don’t have shares that can be sold to attract investors.

That means raising extra capital often depends on personal savings, loans, or bringing in a new partner, which isn’t always easy or quick.

This limitation can make it harder to scale up, expand into new markets, or take advantage of opportunities that require significant investment.

If you’re dreaming big, a partnership might feel a bit restrictive compared to a limited company, where getting outside funding or adding new shareholders is much simpler.

6. The tax side of partnerships

In a partnership, each partner is taxed individually on their share of the profits, just like a self-employed person.

That might sound simple, but it also means there are fewer opportunities to plan and reduce your tax bill compared to a limited company.

For example, limited companies can use strategies such as adjusting salaries, dividends, or pension contributions to manage tax liabilities, which is something partnerships don’t have as much flexibility to do.

Consequently, some partners could end up paying more in personal taxes than they would in a company structure, especially if the business is doing well.

It’s not a deal-breaker, but it’s definitely something to keep in mind before diving into a partnership.

What about National Insurance contributions (NICs)?

As a partner, you’ll pay National Insurance as if you were self-employed:

- Class 2 NICs: A fixed weekly amount if your profits are above £12,570 (for 2025–26)

- Class 4 NICs: 6% on profits between £12,570 and £50,270, plus 2% on anything above £50,270

- How it’s paid: Calculated through your annual self-assessment and paid directly by you

- Employer NICs: Not required, since partners aren’t employees

7. The credibility factor: Perception and prestige

It’s worth thinking about how a partnership comes across to clients, investors, and the wider market.

Unincorporated partnerships, in particular, can sometimes feel a bit ‘less official’ or less professional compared to limited companies.

Part of the reason is transparency. Limited companies have to file accounts with Companies House, so outsiders can easily see how the business is doing.

Partnerships don’t have to do this, which might make some clients or investors hesitant, especially in industries where trust and credibility are key.

This doesn’t mean a partnership can’t thrive, but it’s something to keep in mind because how people perceive your business can affect opportunities, partnerships, or even funding down the line.

8. Exit and succession difficulties

Leaving a partnership isn’t always as simple as handing in your notice.

If one partner wants to exit or sell their share but the others aren’t on board, things can get messy fast.

Without a clear exit strategy in the partnership agreement, disagreements can drag on for months or even force the business to close entirely.

This is why planning for the future is so important.

Partnerships are great for sharing responsibilities and pooling resources, but they also come with challenges, including:

- Unlimited liability,

- Complex decision-making,

- Potential conflicts, and

- General instability.

Thinking ahead and having a well-drafted agreement in place can help protect everyone and make transitions smoother.

By addressing potential issues upfront, the agreement gives clarity on profit-sharing, decision-making, exit strategies, and other tricky situations, helping keep both the business and the relationships between partners on track.

Disadvantages of partnerships: Wrapping it up

Partnerships can be a great way to start a business, offering shared responsibility, combined skills, and the support of a trusted partner.

But they also come from unlimited personal liability and tricky decision-making to exit challenges and credibility concerns.

For many entrepreneurs, these disadvantages can outweigh the benefits, especially if you’re planning to grow, attract investors, or protect your personal assets.

If you’re looking for a structure that offers more legal protection, continuity, and flexibility, a limited company might be a better fit.

This structure protects your personal assets, makes it easier to raise capital, and provides a clearer framework for decision-making and succession, helping you focus on growing your business with peace of mind.

To make the process even smoother, ANNA Money can help with company formation, accounting, and tax management, giving you the tools and guidance to set up your limited company efficiently and stay on top of your finances from day one.

How can ANNA Money take the stress out of starting your business?

ANNA Money is an all-in-one tool for money, invoicing, expenses, bookkeeping and taxes.

Here's how we can help you:

✨ Free company formation: Register your UK limited company with the Companies House fee on us, and open a business account with ANNA at the same time.

✨ Check your desired company name and get suggestions in case it’s already taken.

✨ Same-day registration: Submit your application by 3 PM, and we guarantee your company will be registered and your business account opened by the end of the day.

✨ Comprehensive business tools: Access an all-in-one platform that includes invoicing, receipt scanning, tax filing, and bookkeeping tools to simplify your financial admin.

✨ Get all your taxes covered: Payroll, VAT filing, and Corporation Tax, and make sure you meet the deadlines.

Here’s something you’ll want to hear

ANNA Money is now an official Authorised Corporate Service Provider (ACSP)!

That means we’re fully approved by Companies House to handle identity checks for anyone setting up a UK company.

Becoming an ACSP is a huge milestone for us, and it’s a testament to the trusted, regulated service we’ve already provided to over 16,000 UK businesses.

Simply put, it shows we’re serious about making company formation simple, safe, and reliable for everyone.

Register with ANNA and start your business the smart way.

Read the latest updates

![What Is the Threshold for Making Tax Digital? [Guide]](https://storage.googleapis.com/anna-website-cms-prod/small_cover_3057_f0f2ffd268/small_cover_3057_f0f2ffd268.webp)

![Making Tax Digital for Freelancers [Complete 2026 Guide]](https://storage.googleapis.com/anna-website-cms-prod/small_cover_3000_25_15d6713572/small_cover_3000_25_15d6713572.webp)

![How to Sign Up for Making Tax Digital [A Detailed Guide]](https://storage.googleapis.com/anna-website-cms-prod/small_cover_3031_86f7f6f18a/small_cover_3031_86f7f6f18a.webp)

![MTD ITSA for Landlords [+6 Software Options Compared]](https://storage.googleapis.com/anna-website-cms-prod/small_cover_3025_77131ed4c8/small_cover_3025_77131ed4c8.webp)

![How to Choose the Best MTD Bridging Software [+Comparison]](https://storage.googleapis.com/anna-website-cms-prod/small_cover_3000_22_ba8f9dee9d/small_cover_3000_22_ba8f9dee9d.webp)

You may also like

![Limited Company Advantages and Disadvantages in UK [2025 Guide]](https://storage.googleapis.com/anna-website-cms-prod/small_a_BP_3_Nv_Iq_R_Lda_Bz_Vh_limited_company_advantages_and_disadvantages_bab7f6b99f/small_a_BP_3_Nv_Iq_R_Lda_Bz_Vh_limited_company_advantages_and_disadvantages_bab7f6b99f.png)

![What's the Difference Between Public & Private Limited Company [Explained]](https://storage.googleapis.com/anna-website-cms-prod/small_cover_3000_7_Difference_Between_Public_and_Private_Limited_Company_Explained_7cb4a018ae/small_cover_3000_7_Difference_Between_Public_and_Private_Limited_Company_Explained_7cb4a018ae.webp)

Open a business account in minutes