What is Companies House: Everything UK Business Owners Need to Know

Discover what is Companies House, how it works, why it matters for your business, and what you need to know to stay compliant and informed.

- In this article

- What is Companies House?

- Registering a company: How to incorporate and what you need

- Business structures: Who must register and how they differ

- What information is on the public register?

- Maintaining company compliance: Annual filings and updates

- Consequences of non-compliance (Penalties and dissolution)

- New powers under the Economic Crime and Corporate Transparency Act 2023 (ECCTA)

- Companies House vs HMRC: Understand the difference

- How ANNA helps you run your business smarter

What is Companies House?

Companies House is the United Kingdom’s official registrar of companies. It is a government agency responsible for incorporating new companies, maintaining the public register of companies, and dissolving companies that are no longer active.

The agency keeps records of key company information and makes that information available to the public, which is crucial for transparency and trust in the business community.

Companies House is not a regulator of business activities or a tax authority – its role is to formally record the existence and details of companies and ensure they comply with certain filing requirements under company law.

Registering a company: How to incorporate and what you need

Registering a new company with Companies House is a straightforward process, but it requires careful preparation:

1. Choose a business structure

First, decide on the legal structure of your business (e.g. private limited company, limited liability partnership, etc.). We will discuss the different structures in the next section, but this choice will affect your registration process and obligations.

2. Choose a company name

Pick a unique name for your company. It must not conflict with an existing company’s name and must comply with naming rules (for example, certain words are restricted or require prior permission). You can use the Companies House name availability search to check if your desired name is free, or use ANNA’s free checker below.

A private company limited by shares will typically end in “Ltd” (or “Limited”), whereas a public company ends in “PLC”. Ensure the name isn’t misleading or offensive per Companies House guidelines.

3. Decide on a registered office address

Every company must have an official address, known as the registered office. This address must be in the UK (in the same country your company is registered in: England/Wales, Scotland, or Northern Ireland) and will be publicly visible

Official mail from Companies House and HMRC will be sent here, so it should be an address you can access regularly (many new business owners use their home address or a serviced office address). If you don’t want your address publicly displayed, use ANNA’s virtual address feature.

4. Prepare key details and documents

When registering, you’ll need to provide certain information:

- Director(s) details: At least one director is required for a limited company (must be at least 16 years old). You’ll submit each director’s name, date of birth, nationality, occupation (optional), and a service address.

- Shareholder(s) details: For a company limited by shares, you need at least one shareholder (often the director and shareholder can be the same person). You’ll provide each shareholder’s name and address, and details of the shares they will own. Most small companies start with a single share issued to the founder.

- People with significant control: Apart from directors and shareholders, you must list PSCs, which could include individuals or entities that have substantial control over the company (e.g. owning more than 25% of shares or voting rights). For most small startups, the PSC is just the main shareholder, but this information is required for transparency.

- Company Secretary (if applicable): A company secretary is optional for private companies. If you appoint one, their details (similar to a director’s details) must be given

- SIC code (business activity): You’ll need to specify the nature of your business by choosing a SIC code (Standard Industrial Classification code). This is a short code that categorises your company’s main activity (for example, 62020 for “Information technology consultancy activities”).

- Memorandum and Articles of Association: The memorandum is a short statement signed by all initial shareholders or guarantors agreeing to form the company, and the articles of association are the rules for running the company. If you register online, the standard template (known as “model articles”) can be adopted automatically. If you want to use custom articles, you may need to upload them or file by post.

- Identity and security details: As part of the process, you’ll provide some personal identification details for security (for example, a recent registration may ask for bits of information like mother’s maiden name, town of birth, National Insurance number, etc., to verify identities)

❗Note: With new regulations coming into force, directors and PSCs will soon be required to undergo formal identity verification – more on that later.

5. Submit your Incorporation Application

You can register online through the official Gov.uk portal or via an agent like ANNA. Online registration is typically the fastest and cheapest method, taking as little as 24 hours in many cases.

6. Receive your Company Number and Certificate

Once your application is approved, Companies House will issue a Certificate of Incorporation, which confirms that the company legally exists and shows your company number and date of formation. You will use your company number in many official dealings going forward.

Congratulations – your company is now up and running on the registry!

What happens after you register your company?

After incorporation, Companies House will automatically share some information with HMRC (the UK tax authority).

Specifically, HMRC is notified of the new company and will send a letter with your Unique Taxpayer Reference (UTR) to the registered office, so you can set up your Corporation Tax account.

Keep an eye out for that letter, as you’ll need to follow instructions to register for business taxes separately (more on the HMRC side later).

❗ Practical tip: Ensure all information you provide is accurate and spelt correctly. Any mistakes in the company name or director details could cause delays or require costly corrections later.

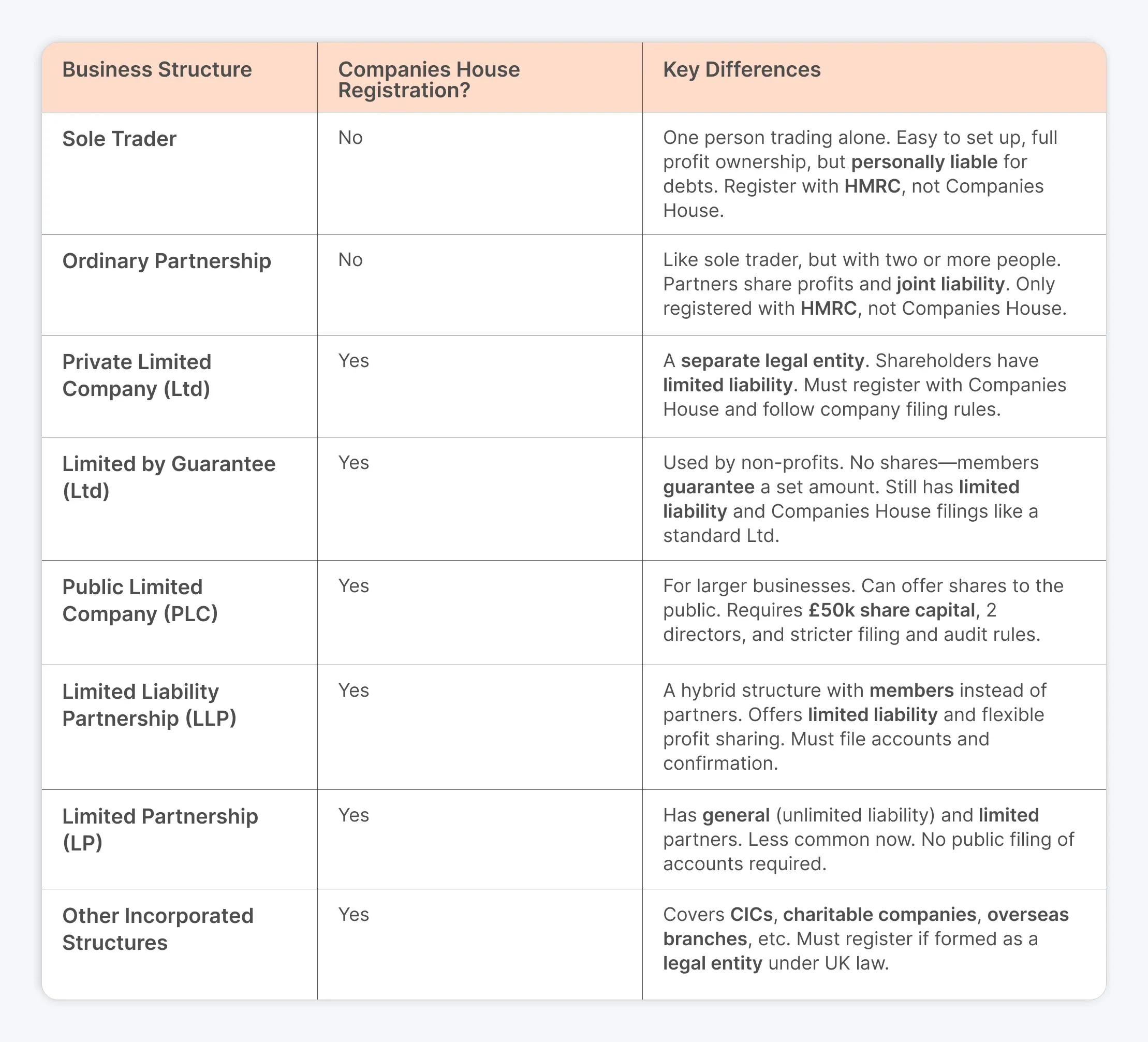

Business structures: Who must register and how they differ

Not every type of business needs to register with Companies House. It depends on your business structure.

As the table shows, only incorporated businesses – those that create a separate legal entity – must register with Companies House. This includes all limited companies (whether limited by shares or guarantee, private or public) as well as LLPs and some less common entities.

Unincorporated businesses like sole traders and ordinary partnerships do not register at Companies House (they simply register with HMRC for tax)

What information is on the public register?

One of Companies House’s core functions is to maintain a public register of company information that anyone can access. This is central to the UK’s corporate transparency regime – it allows people to know who they’re doing business with.

Key information available on the register includes:

1. Company details:

The company’s name, registered number, and date of incorporation. It will also show the company type (for example, “Private Limited Company by shares”, “Limited Liability Partnership”, etc.)

2. Registered Office Address:

The official address of the company (as provided during registration and updated if it changes). While the registered office is public, directors’ residential addresses can be kept off the public record by using a service address. Only the service address appears on the public register in that case.

3. Nature of business:

The SIC code and description of the company’s main business activities.

4. Directors and secretaries:

The names of all current directors and any company secretary, as well as any past directors who have resigned. For individuals, the register will show their name, month and year of birth (not full DOB for privacy), nationality, and service address. It will not show their private home address if a separate service address was provided (except for older records where it might have been used).

5. People with Significant Control (PSC):

The register will list the beneficial owners or controllers of the company – usually the major shareholders or guarantors, or anyone who otherwise exercises significant influence or control. For each PSC, it shows their name, month/year of birth, nationality, country of residence, and the nature of their control (e.g. “owns more than 50% of shares”) on the PSC register. This PSC regime was introduced to increase transparency about who really owns and controls UK companies.

6. Share capital and shareholders:

For companies limited by shares, the public can see the company’s share capital (the number of shares and their nominal value) and a list of shareholders, at least at the time of incorporation and whenever annual returns/confirmation statements update that info. Small private companies often have just one shareholder, so the PSC info covers this. Larger companies may file separate shareholder lists if needed.

7. Financial accounts:

Every year, companies must file their annual financial statements (accounts). These accounts are published on the register for anyone to view. For small companies, these might be abbreviated accounts with limited detail; for larger companies, full accounts are provided. The accounts give insight into the company’s financial health (assets, liabilities, earnings, etc.). Accounts filings are available as PDF documents for download on the Companies House website.

8. Confirmation statements (Annual returns):

The company’s annual confirmation statement (previously known as the annual return) is also on record. This document confirms that the company information is up-to-date each year, including details like directors, shareholders, and PSCs. The latest confirmation statement and date of the next due statement are noted on the register.

9. Filing history:

Perhaps most useful, the register provides a filing history – a list of all documents the company has filed, with dates. You can download copies of these filings (for free) to see the actual forms and documents submitted.

10. Mortgage charges and insolvency:

If the company has taken out secured loans (such as mortgages or charges against its assets), those charges are also recorded on the register. Additionally, any insolvency proceedings (such as those involving liquidation or administration) would be noted.

11. Overseas entities info: (If applicable)

Companies House now also maintains a Register of Overseas Entities, which is a register of foreign companies that own UK property, showing their beneficial owners. This is more relevant if you deal with property or foreign entities, but it’s another aspect of transparency introduced recently.

Maintaining company compliance: Annual filings and updates

Think of incorporation as the start of a responsibility to regularly inform Companies House (and the public register) about your company’s status and any changes. The main recurring obligations are annual filings and event-driven updates:

🔸 Annual accounts:

Every company must file annual financial accounts with Companies House, usually within 9 months of the financial year-end.

For example, if your year ends on March 31, the filing deadline is December 31.

- New companies may have a longer first accounting period.

- Small and micro companies can often submit simplified (abridged or micro-entity) accounts. Filing is free, but missing the deadline results in penalties.

❗Note: Accounts must also be sent to HMRC separately with your tax return.

🔸Confirmation statement:

This is a yearly check-in to confirm your company details (directors, shareholders, etc.) are accurate.

It’s due every 12 months, with a 14-day grace period. You can file more than once a year if needed.

The fee is £34 online (as of 2024), covering all filings in a 12-month period. Failing to file can eventually lead to your company being struck off.

🔸 Event-driven updates:

You must report certain changes to Companies House as they happen. Common examples include:

- Directors/Secretaries: Appointments, resignations, or changes (forms AP01, TM01).

- Registered Office: File form AD01 if you change the address.

- Company Name: Requires a shareholder resolution and form NM01.

- Shares/Ownership: New shares (form SH01), structural changes (SH02, SH03), and new PSCs (People with Significant Control) must be reported within 14 days.

- PSC changes: Use forms PSC01–PSC09 for changes in ownership/control.

- Accounting year-end: File form AA01 to change your accounting reference date.

- Company records location: If using a SAIL address, file AD02 or AD03.

- Other filings: Includes registering charges (MR01), voluntary strike-off (DS01), and more.

Remember, you're responsible for timely and accurate filings. While Companies House doesn’t audit your figures, new rules mean they’re increasingly verifying identity and data.

Consequences of non-compliance (Penalties and dissolution)

Failing to meet your Companies House duties can lead to serious consequences.

As a company director, it’s your legal responsibility to stay compliant. Here's what can happen if you don’t:

🔸 Late filing penalties for accounts:

If you file your company’s annual accounts after the deadline, Companies House automatically issues a fine. The penalty depends on how late you are:

- Up to 1 month late: £150

- 1 to 3 months late: £375

- 3 to 6 months late: £750

- Over 6 months late: £1,500

These fines apply to private companies and LLPs (public company fines are higher).

If you miss the deadline two years in a row, the fine is doubled in the second year.

For example, being one month late two years in a row means paying £150 the first year and £300 the next.

Penalties are fixed by law and rarely waived, so forgetting the deadline or blaming your accountant is not considered a valid excuse.

💡 Pro tip: Simplify your tax life with ANNA +Taxes — it auto-calculates VAT, Corporation Tax, PAYE, and even files your returns. For just £3/month for the first 3 months, you get smart tools like a personalised tax calendar, automated expense sorting, and expert support. Perfect for first-time company owners who want to stay compliant without the stress.

🔸New penalties for other filings (from October 2024):

Until recently, only annual accounts attracted fines. But starting October 2024, Companies House can issue financial penalties for other breaches, like failing to submit confirmation statements or ignoring reminders. The goal is to increase compliance, not to generate revenue, but enforcement will be stricter.

🔸 Strike-off and company dissolution:

If your company repeatedly fails to file accounts or confirmation statements, Companies House may begin strike-off proceedings.

- First, they’ll send warning letters to your registered office. If there’s no response, a notice is published in The Gazette to strike the company off the register.

- If still unresolved, the company is dissolved, meaning it legally ceases to exist. Any assets left in the company are forfeited to the Crown (bona vacantia), and the directors lose the protection of limited liability.

While it's possible to restore a dissolved company, the legal process is costly and time-consuming; it's best to avoid it entirely.

🔸 Director disqualification and criminal liability:

Repeated non-compliance or serious breaches can lead to director disqualification for up to 15 years. This means you're legally banned from managing or directing any UK company during that time. In more serious cases, such as filing false information, criminal charges may apply under the Companies Act. Offenses like knowingly submitting false accounts or PSC details can result in fines, a criminal record, or even imprisonment.

🔸 Business and reputation risks:

All your filing history is public. Late or missing documents show up on the public register and can damage your business’s credibility. Credit reference agencies track this data, so poor compliance may affect your credit score. Customers, suppliers, and investors may also hesitate to work with a company that appears disorganised or non-compliant.

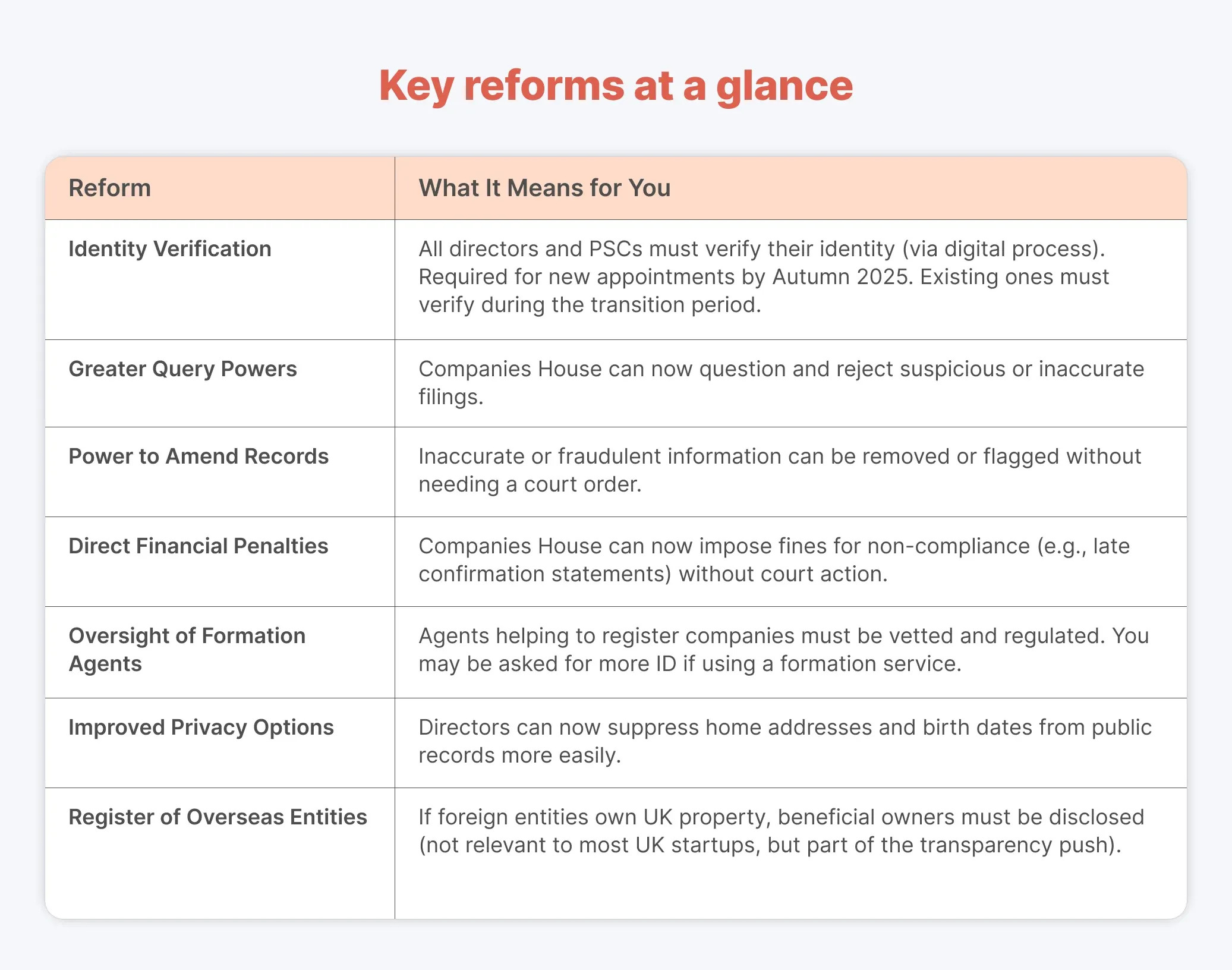

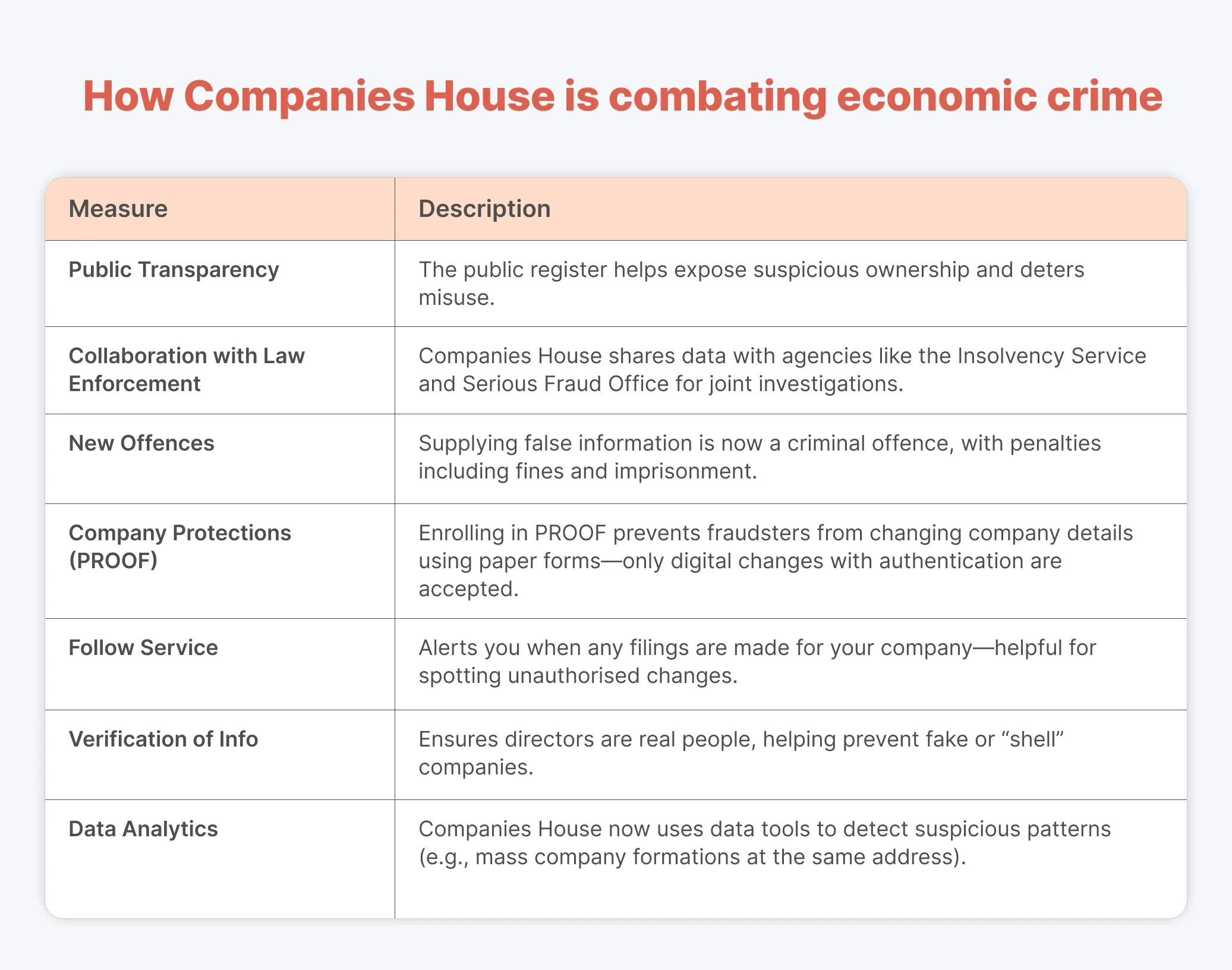

New powers under the Economic Crime and Corporate Transparency Act 2023 (ECCTA)

The ECCTA 2023 significantly expands Companies House's role – from passive record-keeper to active regulator. As a business owner, these changes directly impact how you manage your company filings.

What you should do as a business owner

- Prepare to verify your identity when forming or managing your company.

- Keep your company information accurate and up-to-date.

- Respond promptly to any queries or notices from Companies House.

- Use tools like PROOF and Follow to protect your company from fraud.

- Work only with reputable formation agents.

- Know that Companies House now has the authority and obligation to enforce compliance more actively.

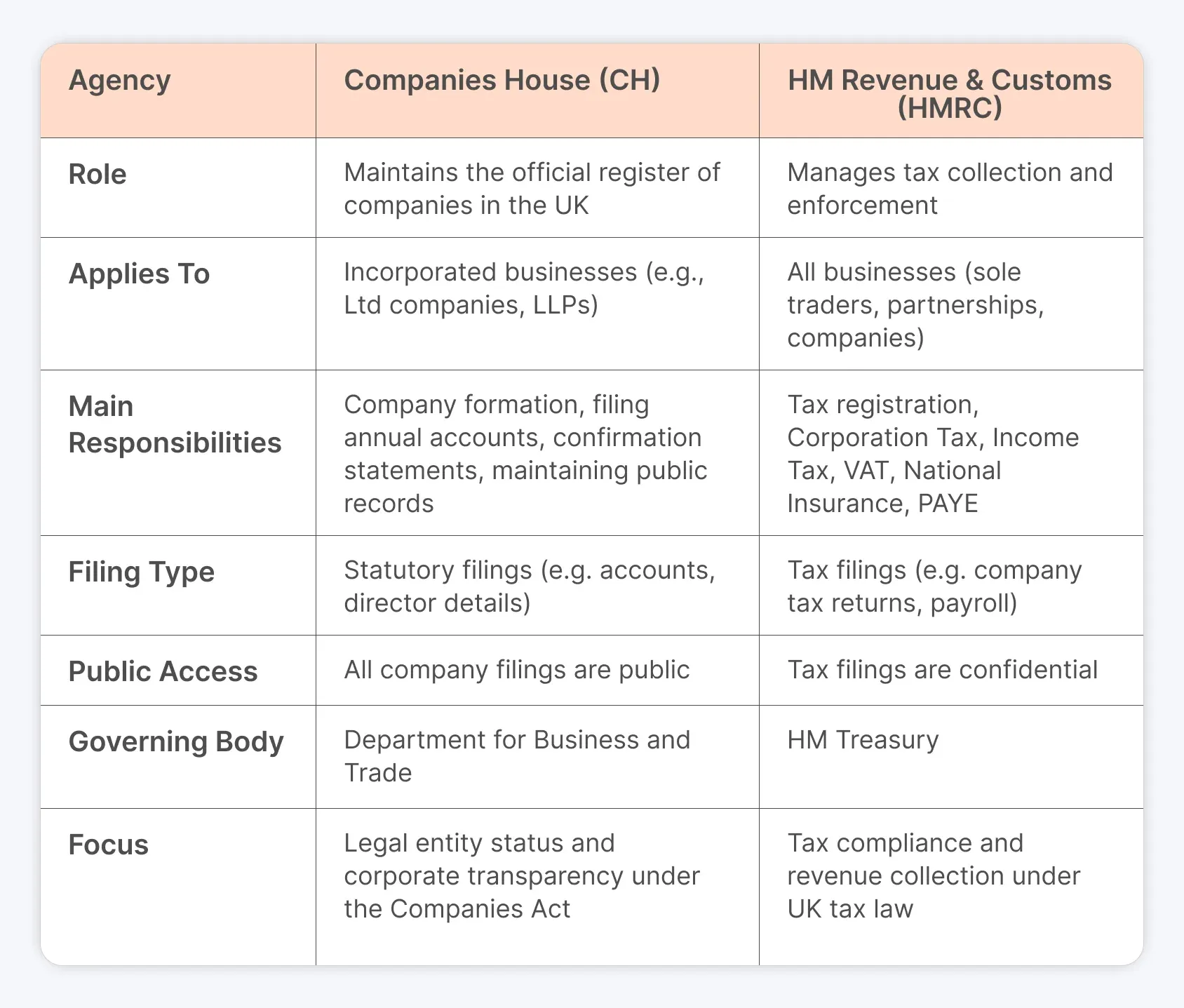

Companies House vs HMRC: Understand the difference

New business owners often confuse Companies House with HMRC (His Majesty’s Revenue & Customs), but they are separate government organisations with very different roles:

To put it succinctly: Companies House is about your company’s legal life, HMRC is about your company’s tax life.

🔸Separate obligations:

It’s possible to be in good standing with Companies House (all filings up to date) but in trouble with HMRC (say, late paying tax or filing tax returns), or vice versa. So you need to manage both. Companies House will dissolve your company for failing to file annual accounts or confirmation statements.

HMRC, on the other hand, could penalise or prosecute you for failing to pay taxes or file tax returns. If Companies House dissolves a company, HMRC may also come knocking because a dissolved company that owed taxes is a problem, so staying compliant with both is essential for your business's health.

🔸 One more distinction:

HMRC for all, Companies House for some. If you operate as a sole trader or ordinary partnership, you only deal with HMRC (there’s no Companies House role).

If you operate as a limited company or LLP, you deal with both agencies. This means more paperwork, but also benefits such as limited liability and possibly tax advantages.

How ANNA helps you run your business smarter

ANNA isn’t just a business account but your financial sidekick.

From registering your company to sorting your taxes, invoicing clients, and managing expenses, ANNA brings all your essential business tools into one smart, easy-to-use platform.

You’ll get:

⚡Fast setup and company registration

⚡A powerful account with cards, pots, and instant payments

⚡Automated accounting and tax filing, including VAT, Corporation Tax, and PAYE

⚡ Real-time insights like a personalised tax calendar, bookkeeping score, and cash flow tools

⚡ Invoicing, expense tracking, and payroll – all in one place

⚡ And so much more!

With expert support available 24/7 and plans starting at just £0/month (plus an optional +Taxes add-on), ANNA helps you save time, stay compliant, and focus on growing your business.

Read the latest updates

![What Is the Threshold for Making Tax Digital? [Guide]](https://storage.googleapis.com/anna-website-cms-prod/small_cover_3057_f0f2ffd268/small_cover_3057_f0f2ffd268.webp)

![Making Tax Digital for Freelancers [Complete 2026 Guide]](https://storage.googleapis.com/anna-website-cms-prod/small_cover_3000_25_15d6713572/small_cover_3000_25_15d6713572.webp)

![How to Sign Up for Making Tax Digital [A Detailed Guide]](https://storage.googleapis.com/anna-website-cms-prod/small_cover_3031_86f7f6f18a/small_cover_3031_86f7f6f18a.webp)

![MTD ITSA for Landlords [+6 Software Options Compared]](https://storage.googleapis.com/anna-website-cms-prod/small_cover_3025_77131ed4c8/small_cover_3025_77131ed4c8.webp)

![How to Choose the Best MTD Bridging Software [+Comparison]](https://storage.googleapis.com/anna-website-cms-prod/small_cover_3000_22_ba8f9dee9d/small_cover_3000_22_ba8f9dee9d.webp)

![How to Change Company Shares on Companies House [Step-by-Step Guide]](https://storage.googleapis.com/anna-website-cms-prod/small_a_EGQI_7h8_WN_L_Vp_c_Cover3000_5201ad5108/small_a_EGQI_7h8_WN_L_Vp_c_Cover3000_5201ad5108.webp)

![What is a registered Office Address? [Comprehensive Guide]](https://storage.googleapis.com/anna-website-cms-prod/small_a_Fwzx_Hfc4b_H_Wiu_QO_cover3000_Whatisa_Registered_Office_Address_cea053dd71/small_a_Fwzx_Hfc4b_H_Wiu_QO_cover3000_Whatisa_Registered_Office_Address_cea053dd71.webp)

![What Is a Dormant Company? Definition, Benefits & Tax Guide [2026]](https://storage.googleapis.com/anna-website-cms-prod/small_Cover3000_What_Isa_Dormant_Company_Definition_Benefits_and_Tax_Guide_2025_a3de366f6b/small_Cover3000_What_Isa_Dormant_Company_Definition_Benefits_and_Tax_Guide_2025_a3de366f6b.webp)

![Offshore Company Registration in the UK [2026 Guide]](https://storage.googleapis.com/anna-website-cms-prod/small_cover_3000_cdb14668f7/small_cover_3000_cdb14668f7.webp)

![How to Get Proof of Address: Easy Ways Explained [2026 Guide]](https://storage.googleapis.com/anna-website-cms-prod/small_cover_3000_How_to_Get_Proof_of_Address_Easy_Ways_Explained_2025_Guide_6849892bd3/small_cover_3000_How_to_Get_Proof_of_Address_Easy_Ways_Explained_2025_Guide_6849892bd3.webp)

![Can You Use a Dissolved Company Name? [Rules Explained]](https://storage.googleapis.com/anna-website-cms-prod/small_cover_3000_Can_You_Use_a_Dissolved_Company_Name_O_Co_Rules_and_Restrictions_Explained_3809e36850/small_cover_3000_Can_You_Use_a_Dissolved_Company_Name_O_Co_Rules_and_Restrictions_Explained_3809e36850.webp)

Open a business account in minutes